“No one in this world, so far as I know – and I have searched the record for years, and employed agents to help me – has ever lost money by underestimating the intelligence of the great masses of the plain people.”

Get your Free

financial review

It was 1999. Your correspondent was a private client portfolio manager at Merrill Lynch in London. Clients were scrambling over each other to buy technology stocks. ‘Giddy’ doesn’t really do the mania justice. ‘Insane’ comes closer to describing the popular mood.

James Glassman and Kevin Hassett had just published a book, Dow 36,000, the title of which speaks for itself. Merrill’s private client management in London had issued a copy to all staff. Could have been worse. They could have made us drink Kool-Aid spiked with cyanide.

AOL was on the cusp of merging with Time Warner in what would become one of the most value-destructive mergers in corporate history.

Boo.com was in the process of burning through $190 million in vain hopes of establishing an online clothing business.

Lastminute.com, an online travel agency, was just about to squeeze through the IPO window in the UK, before that window slammed violently shut behind it.

Pets.com was still selling dogfood on the internet.

As someone with a keen interest in the emerging eco-system of the worldwide web, your correspondent had stumbled on a website called f**kedcompany.com. The basis of the website was to act as a dotcom deadpool – you could nominate ridiculous businesses busily burning through their seed capital, and the more outrageously destructive their flameout, and the more human misery involved as those businesses crashed back to earth, the more points you scored. Over time it developed a second life as a chatroom for VC (Venture Capital) investors, regular investors or their asset managers, and sundry rubberneckers to spread rumour, innuendo and gossip about dotcom businesses and their mayfly shelf-lives.

We still remember the post from somebody calling himself ‘Stanford MBA’.

It was brief and to the point:

“We have stumbled upon the perfect business model. We will lose money on every sale, and we will make up for up it in volume.”

The US satirical news website ‘The Onion’ excelled itself. The same news source that breathlessly reported ‘New branch of Starbucks opens in toilets of existing Starbucks’ also gave the world this gem:

‘Species of blue-green algae announces IPO’

“LAKE ERIE—Seeking to capitalize on the recent IPO rage on Wall Street, Lake Erie-based blue-green algae Anabaena announced Tuesday that it will go public next week with its first-ever stock offering.

“Anabaena, a photosynthesizing, nitrogen-fixing algae with 1999 revenues estimated at $0 billion, will offer 200 million shares on the NASDAQ exchange next Wednesday under the stock symbol ALG. The shares are expected to open in the $47-$49 range.

“This is an extremely attractive investment opportunity that no investor can afford to ignore,” said Carter Stephens, a Shearson Lehman Brothers investment consultant retained by the freshwater-dwelling prokaryote to guide them through the IPO process. “In addition to being the world’s largest producer of oxygen, Anabaena has a strong foothold in many markets other companies find untenable, from tidal spray pools of Lake Michigan to the frozen ponds of Siberia. And with its base of operation constantly expanding, the future for this blue-chip algae looks especially bright.”

“At a press conference Monday, Richard Kollar, the McCann-Erickson advertising executive in charge of marketing and public relations for Anabaena, praised the soon-to-be-public algae.

“Anabaena has been the clear leader in the blue-green-algae field for over 2.5 billion years,” Kollar said. “It’s helped humans breathe a little easier since Day One.”

“Kollar then unveiled the algae’s official advertising slogan: “Anabaena—We Didn’t Make The Atmosphere, We Just Made It Breathable™.”

“Despite the fact that Anabaena has failed to turn a profitable quarter since its founding in the early Proterozoic Era, Wall Street experts said the algae’s good name and substantial liquid holdings should more than compensate.

“For every company that has a successful IPO, there are 10 others that flop,” said Brian Baum, head of online consulting for Ernst & Young. “But blue-green algae has a history of steady nitrogen production, as well as a very strong relationship with fungi, an environmental power player with whom it produces many common lichens. And with the number of living organisms on the planet rising every day, the demand for Anabaena’s many products and byproducts should only grow.”

“Still, many investors said they are unsure whether they would be willing to take even a moderate risk on the stock.

“One thing they’re not saying in the prospectus—and I’ve been through it thoroughly—is that blue-green algae aren’t really algae. They’re cyanobacteria,” said Jeanette MacAlester, a San Francisco-based stockbroker who is strongly advising her clients not to buy ALG. “I don’t know if I’d put my money in any bacteria, let alone one that seems to think it has something to hide.”

“This is definitely a red-flag stock,” Port St. Lucie, FL, day trader Paul Bostock said. “First off, blue-green algae can cause swimmers’ itch. On top of that, if ingested, it can be toxic. I can see the $4 billion lawsuit already.”

“Despite such reservations, as well as a general concern on Wall Street over IPO oversaturation, Anabaena is expected to be a hot property when it makes its bow next week. Market forecasters are predicting an initial market valuation of $9.6 billion, easily eclipsing the stellar December 1998 IPO of Drosophila melanogaster, the common fruit fly.”

So with the benefit of hindsight, all the warning signs were there.

The sell-off that afflicted the G7 stock markets from 2000 was widely seen as a disaster for so-called TMT (Technology; Media; Telecoms). Whatever sector they were in, though, the shares of the most egregiously popular companies simply became unsustainably high – and most of those companies happened to be pure-play dotcoms without any real likelihood of achieving consistent profitability, let alone market dominance.

The fire next time

“God gave Noah the rainbow sign;

No more water, the fire next time.”

- From The Fire Next Time by James Baldwin.

The reason why the market environment is so much scarier than early 2000 from the vantage point of June 2026 is simple. Whereas the millennial bubble was in dotcom stocks and almost nothing else, Bubble 2.0 is in just about everything. It is universal. It goes beyond a segment of the stock market (technology) to take in virtually all of the US stock market, and those of most other developed economies, too.

Worse still, it transcends the asset class of listed equities and has managed to infect global debt markets, and many property markets, as well.

We now face the problem of an “Everything Bubble”.

The explicit overvaluation of bonds is now arguably much worse than that of stocks, in that investment grade bonds now offer little or no margin of safety whatsoever – they are almost guaranteed to lose their value in real terms for anybody choosing to buy them today. The danger is compounded by the regulatory imperative that pension funds and advised private investors hold government bonds because they are deemed “riskless”. That is a sick joke.

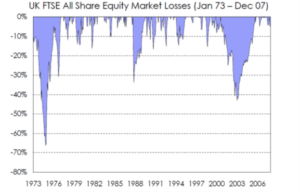

A case in point: the stagflationary 1970s. Courtesy of the Arab oil shocks, the mid-1970s was a disaster for all traditional forms of investment. The following charts relate to the UK market but most western markets would suffer a similar fate over the same period. (Data courtesy of Frontier Capital Management LLP.)

First, the stock market.

In nominal terms, the mid-70s was a dreadful time to own UK stocks.

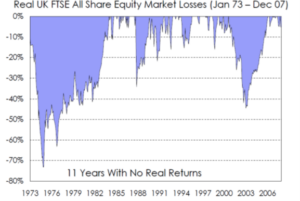

But in real (after-inflation) terms, it was far worse:

An investor who bought UK stocks in 1973 had to wait for 11 years just to break even, after the impact of high inflation.

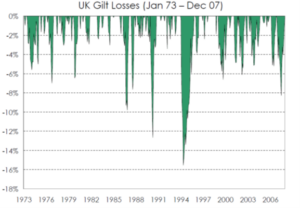

Then there was the bond market.

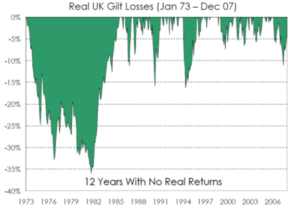

Those downward spikes for bondholders throughout the 1970s look bad enough – until you factor in the real returns, adjusting again for inflation:

For bondholders, the 1970s was an unmitigated disaster. The hapless UK government bond investor in 1973 had to wait until 1985 just to get his money back. An environment of stagnant growth combined with high inflation – which we may yet experience for ourselves – is toxic.

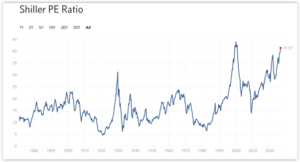

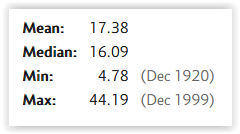

Our favourite metric for assessing the US stock market, referred to here passim, is Robert Shiller’s cyclically adjusted p/e ratio (or CAPE) for the S&P 500 stock index. This takes the 10 year historic average of prior earnings in order simply to smooth out the shorter term price volatility.

US market CAPE ratio – 1880 to 2026

(Source: http://www.multpl.com/shiller-pe/)

The US stock market currently trades on a Shiller p/e of 41.6 versus its long run average of 17.4. Assuming that markets mean revert over time, that suggests that the US market is wildly overvalued relative to a long run average going back 150 years.

For investors today, looking for reasons why the market has remained so abnormally expensive for such an extended period of time may be something of a fool’s errand. In all market matters, the truth is rarely pure and never simple. But the price is the price, and if we don’t respect it, we are likely to be poorly served by casually overpaying to own stuff.

In 1999, the conspicuous bubble was dotcoms. In 2026, it is AI. John Mihaljevic of Latticework and the Manual of Ideas / MOI Global:

“SpaceX has now priced, and the largest IPO in history is no longer hypothetical. The offering has been set, unusually early, at $135 per share, which values the equity at roughly $1.8 trillion, with a final price expected Thursday and the listing scheduled for Friday, June 12. One thing should be clear at the outset: I have the highest respect for Elon Musk as an entrepreneur; on numerous occasions he has achieved the seemingly impossible. His companies have propelled humanity forward and promise to do so in the future.

“I want to be careful about what I am and am not saying. I have no quarrel with what SpaceX might be worth a decade from now; for all I know the answer is enormous. The question that matters for anyone buying on the first day is what the company is worth today, on the strength of its actual financials, its actual markets, and what it actually does. Measured that way, $1.8 trillion reads less like a valuation than like a number the offering has manufactured, and a great deal of machinery has been assembled to bring retail investors into it at the open. Three pieces we are featuring in this week’s deck sharpened how I am thinking about the week ahead, and none of them requires a view on Mars or artificial general intelligence to be useful.

“The first piece, a thought exercise entitled The Stock Market Crash of 2027 by James Emanuel, Mauricio Heck, and Hugo Navarro, presents a structural argument rather than a forecast. Three mega-IPOs, SpaceX, OpenAI, and Anthropic, are arriving inside roughly six months and together reaching toward $4 trillion or more, with Anthropic’s recent private round alone near $1 trillion. The dollars to absorb that supply have to come from somewhere, and the likeliest source is investors trimming the mega-cap technology positions they already hold, since these listings sit in the same bucket. In a market this concentrated in a handful of technology names, that rotation could pull the broad indices down on its own.

“Two design features make the setup more fragile still. SpaceX is bringing only a small fraction of its implied value to market at the start, reportedly 3% to 5% of the equity, which manufactures the scarcity needed to support a price like this in the first place. And the lock-up is not a single 180-day cliff but a staggered series of releases, so across the back half of the year the float swells in tranches and the early scarcity reverses into a flood. The historical rhymes are not comforting. Facebook fell by roughly half after its 2012 lock-up rolled off, and the dot-com unwind was a rolling sequence of expirations rather than a single break. The investors most exposed to that sequence are the ones buying at the open, who pay the engineered price and then inherit the unlock calendar.

“The second piece I include with real respect, and with a disagreement I want to state carefully. Aswath Damodaran revisited his SpaceX valuation once the prospectus was public and arrived at an equity value of about $1.3 trillion, roughly $500 billion, or close to 30%, below the $135 offering. Damodaran is the dean of valuation, and his practice of publishing his full work, spreadsheet included, for anyone to inspect and challenge is a genuine service to the investing community. On the headline point he and I do not actually disagree: even his estimate, which already leans on generous assumptions about the next decade, still lands well below the offering price, which is another way of saying there is no margin of safety for an IPO buyer.

“Where I hesitate to follow is on the prior question, whether a business like this can be valued today with that degree of precision at all.. Damodaran himself flags the prospectus’s claim of a $28 trillion total addressable market, $26 trillion of it in AI, as closer to fantasy than forecast; he then doubles his own AI revenue target, to $160 billion, while trimming the assumed AI operating margin from 45% to 25%, and that single pair of choices moves the answer by a wide margin. When inputs this distant and this uncertain carry most of the result, my own instinct is that the honest output is a range too wide to anchor a decision rather than a single figure. None of this is a criticism of his rigor, which is beyond question; it is a difference about how much any method, however careful, can ask of facts this thin. SpaceX plainly contains valuable businesses. The question is the price today, and on that, his figure and my skepticism point in the same direction.

“The third piece, from Phil Bak, turns to the index providers, and it is the one that genuinely encouraged me. Under heavy pressure to fast-track these mega-IPOs into their benchmarks from day one, several providers, including Nasdaq and FTSE Russell, moved to accommodate. S&P Dow Jones did not. It held to its twelve-month seasoning requirement and its GAAP profitability requirement and declined to make an exception for size, on the principle that financial viability, seasoning, and float standards should not be waived “solely based on market capitalization.” For a company that lost roughly $5 billion last year, that means S&P 500 funds will not be forced to buy SpaceX at any price for a long time. I do not think the stakes here are small.

“Bending the rules to pull an unseasoned, loss-making company into the major indices at a nosebleed valuation would hand the bill to the passive investors least able to absorb it, retirees among them, who never chose the position. That is an abdication of the duty those benchmarks owe the people who entrust them with their savings. S&P is the adult in the room, and if it holds the line it is plainly acting in investors’ interest..

“There are still corners of the market that are reasonably priced, and a few that are outright cheap, so it remains possible to stay fully invested while stepping well clear of the excess on display in this offering.”

In our book, Investing through the Looking Glass, we examine the causes of how we collectively got into this mess. The guilty players all get their own chapter headings, namely:

- The banks

- The central banks

- Economists and financial theorists

- Fund managers.

But rather than offer its readers nothing more than a glass of whisky and a loaded revolver, we also offer solutions to our current predicament. Those respective chapter headings are:

- Value investing

- Trend-following

- Gold.

Value investing in listed stocks – on a global and unconstrained basis – is a core focus for us, unconstrained by geography and business sector, and focussing entirely on bottom up, defensible value. We find especial value in the commodities arena.

But there is no single magic bullet out there. If you don’t know what’s ahead but you fear for the worst (which we do), it makes sense to diversify as widely as possible.

What is different this time is the general mood. In 2000, the air was electric with the hopes and dreams of a new era, as ridiculous as they now seem with hindsight. But here in 2026, we are living through what is surely the tail end of one of the most reviled (and narrow) bull markets in history. Nothing feels quite real – which is what happens after you allow a bunch of unelected bureaucrats at the world’s central banks to play unlimited games with the monetary system.

The single most important characteristic of any investment you make is its starting valuation when you buy it. Nothing else comes close.

The valuations of most stock markets are close to, or at, record highs.

The valuations of most bond markets are close to record highs – when the supply, and rate of expansion, of sovereign debt has never been higher.

Central bankers like to believe that it’s impossible to identify bubbles before they burst. With all the respect due to them – i.e. none whatsoever – that is nonsense. It was evident to many in early 2000 that the market had got ahead of itself.

Quite likely, this will soon be one of the best times in history to be a value investor – whether in relative, or absolute terms. We may be wrong – QE and ZIRP have been with us for well over a decade now – but we sense a disturbance in the force, as bonds, stocks and property prices all creak under the accumulated pressure of an over-a-decade-long foray into absurdity.

In the days of ancient Rome, it is said that during a triumphal procession, a military commander would be accompanied by an Auriga – a slave who would stand behind him, whispering in his ear Memento homo: remember, you too are mortal.

Someday, perhaps quite soon, this bull market in everything is going to end. Now is probably a good time to be raising cash – and, of course, to be concentrating on stocks possessing what Benjamin Graham would have called a “margin of safety”. If many of those stocks are to be found outside the US market pressure cooker, so be it.

Last words this week should probably go, then, to Warren Buffett:

“Cash combined with courage in a crisis is priceless.”

And also to Lord Overstone:

“No warning on earth can save people determined to grow suddenly rich.”

………….

As you may know, we also manage bespoke investment portfolios for private clients internationally. We would be delighted to help you too. Because of the current heightened market volatility we are offering a completely free financial review, with no strings attached, to see if our value-oriented approach might benefit your portfolio – with no obligation at all:

Get your Free

financial review

…………

Tim Price is co-manager of the VT Price Value Portfolio and author of ‘Investing through the Looking Glass: a rational guide to irrational financial markets’. You can access a full archive of these weekly investment commentaries here. You can listen to our regular ‘State of the Markets’ podcasts, with Paul Rodriguez of ThinkTrading.com, here. Email us: info@pricevaluepartners.com.

Price Value Partners manage investment portfolios for private clients. We also manage the VT Price Value Portfolio, an unconstrained global fund investing in Benjamin Graham-style value stocks and real assets, and also in systematic trend-following funds.

“No one in this world, so far as I know – and I have searched the record for years, and employed agents to help me – has ever lost money by underestimating the intelligence of the great masses of the plain people.”

Get your Free

financial review

It was 1999. Your correspondent was a private client portfolio manager at Merrill Lynch in London. Clients were scrambling over each other to buy technology stocks. ‘Giddy’ doesn’t really do the mania justice. ‘Insane’ comes closer to describing the popular mood.

James Glassman and Kevin Hassett had just published a book, Dow 36,000, the title of which speaks for itself. Merrill’s private client management in London had issued a copy to all staff. Could have been worse. They could have made us drink Kool-Aid spiked with cyanide.

AOL was on the cusp of merging with Time Warner in what would become one of the most value-destructive mergers in corporate history.

Boo.com was in the process of burning through $190 million in vain hopes of establishing an online clothing business.

Lastminute.com, an online travel agency, was just about to squeeze through the IPO window in the UK, before that window slammed violently shut behind it.

Pets.com was still selling dogfood on the internet.

As someone with a keen interest in the emerging eco-system of the worldwide web, your correspondent had stumbled on a website called f**kedcompany.com. The basis of the website was to act as a dotcom deadpool – you could nominate ridiculous businesses busily burning through their seed capital, and the more outrageously destructive their flameout, and the more human misery involved as those businesses crashed back to earth, the more points you scored. Over time it developed a second life as a chatroom for VC (Venture Capital) investors, regular investors or their asset managers, and sundry rubberneckers to spread rumour, innuendo and gossip about dotcom businesses and their mayfly shelf-lives.

We still remember the post from somebody calling himself ‘Stanford MBA’.

It was brief and to the point:

“We have stumbled upon the perfect business model. We will lose money on every sale, and we will make up for up it in volume.”

The US satirical news website ‘The Onion’ excelled itself. The same news source that breathlessly reported ‘New branch of Starbucks opens in toilets of existing Starbucks’ also gave the world this gem:

‘Species of blue-green algae announces IPO’

“LAKE ERIE—Seeking to capitalize on the recent IPO rage on Wall Street, Lake Erie-based blue-green algae Anabaena announced Tuesday that it will go public next week with its first-ever stock offering.

“Anabaena, a photosynthesizing, nitrogen-fixing algae with 1999 revenues estimated at $0 billion, will offer 200 million shares on the NASDAQ exchange next Wednesday under the stock symbol ALG. The shares are expected to open in the $47-$49 range.

“This is an extremely attractive investment opportunity that no investor can afford to ignore,” said Carter Stephens, a Shearson Lehman Brothers investment consultant retained by the freshwater-dwelling prokaryote to guide them through the IPO process. “In addition to being the world’s largest producer of oxygen, Anabaena has a strong foothold in many markets other companies find untenable, from tidal spray pools of Lake Michigan to the frozen ponds of Siberia. And with its base of operation constantly expanding, the future for this blue-chip algae looks especially bright.”

“At a press conference Monday, Richard Kollar, the McCann-Erickson advertising executive in charge of marketing and public relations for Anabaena, praised the soon-to-be-public algae.

“Anabaena has been the clear leader in the blue-green-algae field for over 2.5 billion years,” Kollar said. “It’s helped humans breathe a little easier since Day One.”

“Kollar then unveiled the algae’s official advertising slogan: “Anabaena—We Didn’t Make The Atmosphere, We Just Made It Breathable™.”

“Despite the fact that Anabaena has failed to turn a profitable quarter since its founding in the early Proterozoic Era, Wall Street experts said the algae’s good name and substantial liquid holdings should more than compensate.

“For every company that has a successful IPO, there are 10 others that flop,” said Brian Baum, head of online consulting for Ernst & Young. “But blue-green algae has a history of steady nitrogen production, as well as a very strong relationship with fungi, an environmental power player with whom it produces many common lichens. And with the number of living organisms on the planet rising every day, the demand for Anabaena’s many products and byproducts should only grow.”

“Still, many investors said they are unsure whether they would be willing to take even a moderate risk on the stock.

“One thing they’re not saying in the prospectus—and I’ve been through it thoroughly—is that blue-green algae aren’t really algae. They’re cyanobacteria,” said Jeanette MacAlester, a San Francisco-based stockbroker who is strongly advising her clients not to buy ALG. “I don’t know if I’d put my money in any bacteria, let alone one that seems to think it has something to hide.”

“This is definitely a red-flag stock,” Port St. Lucie, FL, day trader Paul Bostock said. “First off, blue-green algae can cause swimmers’ itch. On top of that, if ingested, it can be toxic. I can see the $4 billion lawsuit already.”

“Despite such reservations, as well as a general concern on Wall Street over IPO oversaturation, Anabaena is expected to be a hot property when it makes its bow next week. Market forecasters are predicting an initial market valuation of $9.6 billion, easily eclipsing the stellar December 1998 IPO of Drosophila melanogaster, the common fruit fly.”

So with the benefit of hindsight, all the warning signs were there.

The sell-off that afflicted the G7 stock markets from 2000 was widely seen as a disaster for so-called TMT (Technology; Media; Telecoms). Whatever sector they were in, though, the shares of the most egregiously popular companies simply became unsustainably high – and most of those companies happened to be pure-play dotcoms without any real likelihood of achieving consistent profitability, let alone market dominance.

The fire next time

“God gave Noah the rainbow sign;

No more water, the fire next time.”

The reason why the market environment is so much scarier than early 2000 from the vantage point of June 2026 is simple. Whereas the millennial bubble was in dotcom stocks and almost nothing else, Bubble 2.0 is in just about everything. It is universal. It goes beyond a segment of the stock market (technology) to take in virtually all of the US stock market, and those of most other developed economies, too.

Worse still, it transcends the asset class of listed equities and has managed to infect global debt markets, and many property markets, as well.

We now face the problem of an “Everything Bubble”.

The explicit overvaluation of bonds is now arguably much worse than that of stocks, in that investment grade bonds now offer little or no margin of safety whatsoever – they are almost guaranteed to lose their value in real terms for anybody choosing to buy them today. The danger is compounded by the regulatory imperative that pension funds and advised private investors hold government bonds because they are deemed “riskless”. That is a sick joke.

A case in point: the stagflationary 1970s. Courtesy of the Arab oil shocks, the mid-1970s was a disaster for all traditional forms of investment. The following charts relate to the UK market but most western markets would suffer a similar fate over the same period. (Data courtesy of Frontier Capital Management LLP.)

First, the stock market.

In nominal terms, the mid-70s was a dreadful time to own UK stocks.

But in real (after-inflation) terms, it was far worse:

An investor who bought UK stocks in 1973 had to wait for 11 years just to break even, after the impact of high inflation.

Then there was the bond market.

Those downward spikes for bondholders throughout the 1970s look bad enough – until you factor in the real returns, adjusting again for inflation:

For bondholders, the 1970s was an unmitigated disaster. The hapless UK government bond investor in 1973 had to wait until 1985 just to get his money back. An environment of stagnant growth combined with high inflation – which we may yet experience for ourselves – is toxic.

Our favourite metric for assessing the US stock market, referred to here passim, is Robert Shiller’s cyclically adjusted p/e ratio (or CAPE) for the S&P 500 stock index. This takes the 10 year historic average of prior earnings in order simply to smooth out the shorter term price volatility.

US market CAPE ratio – 1880 to 2026

(Source: http://www.multpl.com/shiller-pe/)

The US stock market currently trades on a Shiller p/e of 41.6 versus its long run average of 17.4. Assuming that markets mean revert over time, that suggests that the US market is wildly overvalued relative to a long run average going back 150 years.

For investors today, looking for reasons why the market has remained so abnormally expensive for such an extended period of time may be something of a fool’s errand. In all market matters, the truth is rarely pure and never simple. But the price is the price, and if we don’t respect it, we are likely to be poorly served by casually overpaying to own stuff.

In 1999, the conspicuous bubble was dotcoms. In 2026, it is AI. John Mihaljevic of Latticework and the Manual of Ideas / MOI Global:

“SpaceX has now priced, and the largest IPO in history is no longer hypothetical. The offering has been set, unusually early, at $135 per share, which values the equity at roughly $1.8 trillion, with a final price expected Thursday and the listing scheduled for Friday, June 12. One thing should be clear at the outset: I have the highest respect for Elon Musk as an entrepreneur; on numerous occasions he has achieved the seemingly impossible. His companies have propelled humanity forward and promise to do so in the future.

“I want to be careful about what I am and am not saying. I have no quarrel with what SpaceX might be worth a decade from now; for all I know the answer is enormous. The question that matters for anyone buying on the first day is what the company is worth today, on the strength of its actual financials, its actual markets, and what it actually does. Measured that way, $1.8 trillion reads less like a valuation than like a number the offering has manufactured, and a great deal of machinery has been assembled to bring retail investors into it at the open. Three pieces we are featuring in this week’s deck sharpened how I am thinking about the week ahead, and none of them requires a view on Mars or artificial general intelligence to be useful.

“The first piece, a thought exercise entitled The Stock Market Crash of 2027 by James Emanuel, Mauricio Heck, and Hugo Navarro, presents a structural argument rather than a forecast. Three mega-IPOs, SpaceX, OpenAI, and Anthropic, are arriving inside roughly six months and together reaching toward $4 trillion or more, with Anthropic’s recent private round alone near $1 trillion. The dollars to absorb that supply have to come from somewhere, and the likeliest source is investors trimming the mega-cap technology positions they already hold, since these listings sit in the same bucket. In a market this concentrated in a handful of technology names, that rotation could pull the broad indices down on its own.

“Two design features make the setup more fragile still. SpaceX is bringing only a small fraction of its implied value to market at the start, reportedly 3% to 5% of the equity, which manufactures the scarcity needed to support a price like this in the first place. And the lock-up is not a single 180-day cliff but a staggered series of releases, so across the back half of the year the float swells in tranches and the early scarcity reverses into a flood. The historical rhymes are not comforting. Facebook fell by roughly half after its 2012 lock-up rolled off, and the dot-com unwind was a rolling sequence of expirations rather than a single break. The investors most exposed to that sequence are the ones buying at the open, who pay the engineered price and then inherit the unlock calendar.

“The second piece I include with real respect, and with a disagreement I want to state carefully. Aswath Damodaran revisited his SpaceX valuation once the prospectus was public and arrived at an equity value of about $1.3 trillion, roughly $500 billion, or close to 30%, below the $135 offering. Damodaran is the dean of valuation, and his practice of publishing his full work, spreadsheet included, for anyone to inspect and challenge is a genuine service to the investing community. On the headline point he and I do not actually disagree: even his estimate, which already leans on generous assumptions about the next decade, still lands well below the offering price, which is another way of saying there is no margin of safety for an IPO buyer.

“Where I hesitate to follow is on the prior question, whether a business like this can be valued today with that degree of precision at all.. Damodaran himself flags the prospectus’s claim of a $28 trillion total addressable market, $26 trillion of it in AI, as closer to fantasy than forecast; he then doubles his own AI revenue target, to $160 billion, while trimming the assumed AI operating margin from 45% to 25%, and that single pair of choices moves the answer by a wide margin. When inputs this distant and this uncertain carry most of the result, my own instinct is that the honest output is a range too wide to anchor a decision rather than a single figure. None of this is a criticism of his rigor, which is beyond question; it is a difference about how much any method, however careful, can ask of facts this thin. SpaceX plainly contains valuable businesses. The question is the price today, and on that, his figure and my skepticism point in the same direction.

“The third piece, from Phil Bak, turns to the index providers, and it is the one that genuinely encouraged me. Under heavy pressure to fast-track these mega-IPOs into their benchmarks from day one, several providers, including Nasdaq and FTSE Russell, moved to accommodate. S&P Dow Jones did not. It held to its twelve-month seasoning requirement and its GAAP profitability requirement and declined to make an exception for size, on the principle that financial viability, seasoning, and float standards should not be waived “solely based on market capitalization.” For a company that lost roughly $5 billion last year, that means S&P 500 funds will not be forced to buy SpaceX at any price for a long time. I do not think the stakes here are small.

“Bending the rules to pull an unseasoned, loss-making company into the major indices at a nosebleed valuation would hand the bill to the passive investors least able to absorb it, retirees among them, who never chose the position. That is an abdication of the duty those benchmarks owe the people who entrust them with their savings. S&P is the adult in the room, and if it holds the line it is plainly acting in investors’ interest..

“There are still corners of the market that are reasonably priced, and a few that are outright cheap, so it remains possible to stay fully invested while stepping well clear of the excess on display in this offering.”

In our book, Investing through the Looking Glass, we examine the causes of how we collectively got into this mess. The guilty players all get their own chapter headings, namely:

But rather than offer its readers nothing more than a glass of whisky and a loaded revolver, we also offer solutions to our current predicament. Those respective chapter headings are:

Value investing in listed stocks – on a global and unconstrained basis – is a core focus for us, unconstrained by geography and business sector, and focussing entirely on bottom up, defensible value. We find especial value in the commodities arena.

But there is no single magic bullet out there. If you don’t know what’s ahead but you fear for the worst (which we do), it makes sense to diversify as widely as possible.

What is different this time is the general mood. In 2000, the air was electric with the hopes and dreams of a new era, as ridiculous as they now seem with hindsight. But here in 2026, we are living through what is surely the tail end of one of the most reviled (and narrow) bull markets in history. Nothing feels quite real – which is what happens after you allow a bunch of unelected bureaucrats at the world’s central banks to play unlimited games with the monetary system.

The single most important characteristic of any investment you make is its starting valuation when you buy it. Nothing else comes close.

The valuations of most stock markets are close to, or at, record highs.

The valuations of most bond markets are close to record highs – when the supply, and rate of expansion, of sovereign debt has never been higher.

Central bankers like to believe that it’s impossible to identify bubbles before they burst. With all the respect due to them – i.e. none whatsoever – that is nonsense. It was evident to many in early 2000 that the market had got ahead of itself.

Quite likely, this will soon be one of the best times in history to be a value investor – whether in relative, or absolute terms. We may be wrong – QE and ZIRP have been with us for well over a decade now – but we sense a disturbance in the force, as bonds, stocks and property prices all creak under the accumulated pressure of an over-a-decade-long foray into absurdity.

In the days of ancient Rome, it is said that during a triumphal procession, a military commander would be accompanied by an Auriga – a slave who would stand behind him, whispering in his ear Memento homo: remember, you too are mortal.

Someday, perhaps quite soon, this bull market in everything is going to end. Now is probably a good time to be raising cash – and, of course, to be concentrating on stocks possessing what Benjamin Graham would have called a “margin of safety”. If many of those stocks are to be found outside the US market pressure cooker, so be it.

Last words this week should probably go, then, to Warren Buffett:

“Cash combined with courage in a crisis is priceless.”

And also to Lord Overstone:

“No warning on earth can save people determined to grow suddenly rich.”

………….

As you may know, we also manage bespoke investment portfolios for private clients internationally. We would be delighted to help you too. Because of the current heightened market volatility we are offering a completely free financial review, with no strings attached, to see if our value-oriented approach might benefit your portfolio – with no obligation at all:

Get your Free

financial review

…………

Tim Price is co-manager of the VT Price Value Portfolio and author of ‘Investing through the Looking Glass: a rational guide to irrational financial markets’. You can access a full archive of these weekly investment commentaries here. You can listen to our regular ‘State of the Markets’ podcasts, with Paul Rodriguez of ThinkTrading.com, here. Email us: info@pricevaluepartners.com.

Price Value Partners manage investment portfolios for private clients. We also manage the VT Price Value Portfolio, an unconstrained global fund investing in Benjamin Graham-style value stocks and real assets, and also in systematic trend-following funds.

Take a closer look

Take a look at the data of our investments and see what makes us different.

LOOK CLOSERSubscribe

Sign up for the latest news on investments and market insights.

KEEP IN TOUCHContact us

In order to find out more about PVP please get in touch with our team.

CONTACT USTim Price