“No one is willing to believe that adults too, like children, wander about this earth in a daze and, like children, do not know where they come from or where they are going, act as rarely as they do according to genuine motives, and are as thoroughly governed as they are by biscuits and cake and the rod.”

- Johann Wolfgang von Goethe, ‘The Sorrows of Young Werther’.

Get your Free

financial review

John Vaillant’s ‘The Tiger’ is set in the far eastern Russian wilderness of a region that the Chinese call the ‘forest sea’. It tells the true-life story of an experienced trapper and poacher killed by a tiger, and of the man employed by a unit called ‘Inspection Tiger’ who is brought in to investigate. In some respects it is a “murder mystery written in snow”. It is also a study in human psychology:

“The most terrifying and important test for a human being is to be in absolute isolation…A human being is a very social creature, and ninety percent of what he does is done only because other people are watching. Alone, with no witnesses, he starts to learn about himself—who is he really? Sometimes, this brings staggering discoveries. Because nobody’s watching, you can easily become an animal: it is not necessary to shave, or to wash, or to keep your winter quarters clean—you can live in shit and no one will see. You can shoot tigers, or choose not to shoot. You can run in fear and nobody will know. You have to have something—some force, which allows and helps you to survive without witnesses…Once you have passed the solitude test you have absolute confidence in yourself, and there is nothing that can break you afterward.”

There is something almost mythical in the challenge of contrarian investing. Because at heart, all value investing is contrarian investing. Human beings are hard-wired to seek consensus. For most of our evolutionary history, it made complete sense to be part of the crowd. To be different from the crowd, to go one’s own way, would have been fatal to our ancient ancestors. It would have meant starvation, and a quick, lonely death. In the modern world, perversely, perhaps the financial markets are one of the few places we can still forge an identity for ourselves in the wilderness – a place where we can be alone, yet remain within the crowd. In any event, contrarian investing demands that we be “alone” for much of the time. The value investor Patrick O’Shaughnessy cites the American writer and mythologist Joseph Campbell:

“The cave you fear to enter holds the treasure you seek.”

The business of professional value investing is doubly challenging, in that it involves not just a deep commitment to contrarian investing on the part of the manager, but on the part of his clients, too. In other words, there are two separate entities that have to be completely happy with the adoption of a non-consensual investment policy, namely portfolio manager and client. There’s an old market saying that touches on some of these psychological issues:

If you don’t know who you are, the market is an expensive place to find out.

It may be easy to pay lip service to contrarian investing, but maintaining that commitment in a tough market is anything but. In the words of the German military strategist Helmuth von Moltke, no battle plan survives contact with the enemy.

Here’s a fascinating real world example, sent to us by a friend in South Africa, Kokkie Kooyman.

Imagine you are a shareholder in Warren Buffett’s legendary holding company, Berkshire Hathaway. You’ve already enjoyed some fabulous returns, having tagged along on Buffett’s coattails ever since he started his first partnership in 1956.

It is now 1975.

In 1971, you had $10,000 invested in Berkshire Hathaway stock. You have a friend who had an identical amount invested in the S&P 500 stock index.

Then the Arab oil embargo happens. The oil price soars from $3 a barrel to nearly $12. The stock market collapses. Berkshire is not immune. By 1974, your Berkshire shares are worth $5,708. Your friend is doing badly, but better than you – his investment is worth $7,456.

Now, in 1975, you begin to reassess your portfolio. Your friend has bounced back into the black. His grubstake in the S&P 500 is back above $10,000. But your shares in Berkshire are now almost half of what they were worth four years ago. The stock market has recovered, but your shareholding hasn’t. Ask yourself honestly. What would you have done ?

We suspect that in 1975, most investors would have bailed on Buffett. Underperformance relative to the market for one calendar year is difficult enough to stomach. But sitting through four years of relative underperformance is a really tough ask. Not many investors, we suggest, would have had the stamina.

Selling Berkshire in 1975, of course, would have been a colossal mistake, with the benefit of hindsight. Within just a year, the value of the Berkshire holding would have been above that of the S&P 500 again, and back above the level of your friend’s portfolio. And by 1991, the scale of the subsequent outperformance would have been clear to all. But ask yourself again:

Would you have sold in ’75 ?

Buffett’s mentor, Ben Graham, nicely summarised these problems with his trademark brevity:

“Individuals who cannot master their emotions are ill-suited to profit from the investment process.”

Contrarian investing today is arguably even more of a challenge because it’s damnably difficult to trust the prices of any financial assets, anywhere. How can one invest rationally when all the benchmarks associated with sound investment principles have become hopelessly distorted by central bank stimulus – or by too many asset gatherers slavishly aping the composition of global institutional indices ?

Conventional investment theory holds that the investment journey begins with the “risk-free rate”: the market interest rate available on short term government debt of the highest quality. Investors can, in theory, choose to park their money in “riskless” bank deposits or “riskless” short term government bonds. If they have a higher appetite for risk, they should be able to earn a spread above the risk-free rate by holding bonds of inferior credit quality (corporate debt, for example) or by buying listed equity investments instead.

There are at least two problems with this theory today. One is that the market interest rate is no longer set by anything approximating to a free market. It is set by government fiat. Or more accurately, it is set by central banks, acting as agents for those same governments.

The second is that courtesy of the price distortion inherent in Quantitative Easing and overmuch index tracking, the risk-free returns once offered by government bonds have become return-free risks. An example. Last week it emerged that the Bank of England had just sold £675 million of its UK government bond holdings. The worst sale was of the 2061 Gilt which it started buying at a price of 100 and finally sold last week at a price of £23.41.

There is a third problem. “Risk-free” implies some kind of inherent creditworthiness. But in our Alice-Through-The-Looking-Glass investment world, government bonds now struggle to offer positive real yields even as the supply of government debt has never been higher. It is as if the laws of supply and demand have been utterly rescinded. In other words, the true credit quality of western government debt has never been lower – the exact opposite of what those optically low-seeming yields would suggest.

With politicians throughout the West unable or unwilling to implement the hard choices and economic restructuring required to drag their economies out of a debt-soaked deflationary mire, central bankers have chosen to fill the resultant policy vacuum. But their policy options are limited to playing games with interest rates and money. In the absence of bold political action, central banks were allowed to create ex nihilo money and used it to buy bonds. The somewhat tenuous argument in justification of QE was that it was needed to prevent deflation. Deflation must be defeated because if it becomes entrenched, it will bankrupt heavily indebted governments. There is no evidence yet that QE has been or will be successful to this reflationary end. But there is overwhelming evidence that QE ended up gravely distorting asset prices, and succeeded in driving both bond and equity markets to levels that they may well not have reached in the absence of money-printing.

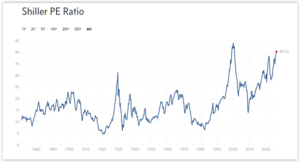

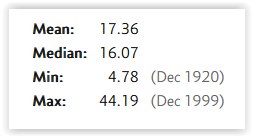

Robert Shiller’s cyclically adjusted price / earnings ratio for the US stock market (or CAPE) provides a sobering perspective on US equity valuations (with the US accounting for over 70% of the MSCI World Equity Index). It offers a 10 year smoothed average of the US market’s p/e multiple.

Shiller P/E, 1880 to 2026

Source: http://www.multpl.com/shiller-pe/

As you can see from the chart, with a current multiple of over 40 times, the Shiller p/e stands at over twice its long run average of 17.4. (A caveat required here is that the Shiller p/e is not particularly useful as an aid for market timing: as the late 1990s experience shows, the stock market can remain, with hindsight, fundamentally overvalued for quite extensive periods.)

All of which makes us despair at the growing number of individuals flooding into the market indiscriminately today, by buying passive ETFs (Exchange Traded Funds), at what are close to all-time highs.

But there’s the stock market, and then there’s the market for individual stocks. While the ongoing crisis in the Middle East virtually guarantees messily high inflation if not stagflation throughout the developed world, we are finding no shortage of attractively priced listed companies in the commodities arena which stand to benefit from an increasingly broad-based commodities rally. It’s an ill wind that blows nobody any good. The question investors must ask is whether they are man enough to detach from the herd and seize the opportunities within the cave.

………….

As you may know, we also manage bespoke investment portfolios for private clients internationally. We would be delighted to help you too. Because of the current heightened market volatility we are offering a completely free financial review, with no strings attached, to see if our value-oriented approach might benefit your portfolio – with no obligation at all:

Get your Free

financial review

…………

Tim Price is co-manager of the VT Price Value Portfolio and author of ‘Investing through the Looking Glass: a rational guide to irrational financial markets’. You can access a full archive of these weekly investment commentaries here. You can listen to our regular ‘State of the Markets’ podcasts, with Paul Rodriguez of ThinkTrading.com, here. Email us: info@pricevaluepartners.com.

Price Value Partners manage investment portfolios for private clients. We also manage the VT Price Value Portfolio, an unconstrained global fund investing in Benjamin Graham-style value stocks and real assets, and also in systematic trend-following funds.

“No one is willing to believe that adults too, like children, wander about this earth in a daze and, like children, do not know where they come from or where they are going, act as rarely as they do according to genuine motives, and are as thoroughly governed as they are by biscuits and cake and the rod.”

Get your Free

financial review

John Vaillant’s ‘The Tiger’ is set in the far eastern Russian wilderness of a region that the Chinese call the ‘forest sea’. It tells the true-life story of an experienced trapper and poacher killed by a tiger, and of the man employed by a unit called ‘Inspection Tiger’ who is brought in to investigate. In some respects it is a “murder mystery written in snow”. It is also a study in human psychology:

“The most terrifying and important test for a human being is to be in absolute isolation…A human being is a very social creature, and ninety percent of what he does is done only because other people are watching. Alone, with no witnesses, he starts to learn about himself—who is he really? Sometimes, this brings staggering discoveries. Because nobody’s watching, you can easily become an animal: it is not necessary to shave, or to wash, or to keep your winter quarters clean—you can live in shit and no one will see. You can shoot tigers, or choose not to shoot. You can run in fear and nobody will know. You have to have something—some force, which allows and helps you to survive without witnesses…Once you have passed the solitude test you have absolute confidence in yourself, and there is nothing that can break you afterward.”

There is something almost mythical in the challenge of contrarian investing. Because at heart, all value investing is contrarian investing. Human beings are hard-wired to seek consensus. For most of our evolutionary history, it made complete sense to be part of the crowd. To be different from the crowd, to go one’s own way, would have been fatal to our ancient ancestors. It would have meant starvation, and a quick, lonely death. In the modern world, perversely, perhaps the financial markets are one of the few places we can still forge an identity for ourselves in the wilderness – a place where we can be alone, yet remain within the crowd. In any event, contrarian investing demands that we be “alone” for much of the time. The value investor Patrick O’Shaughnessy cites the American writer and mythologist Joseph Campbell:

“The cave you fear to enter holds the treasure you seek.”

The business of professional value investing is doubly challenging, in that it involves not just a deep commitment to contrarian investing on the part of the manager, but on the part of his clients, too. In other words, there are two separate entities that have to be completely happy with the adoption of a non-consensual investment policy, namely portfolio manager and client. There’s an old market saying that touches on some of these psychological issues:

If you don’t know who you are, the market is an expensive place to find out.

It may be easy to pay lip service to contrarian investing, but maintaining that commitment in a tough market is anything but. In the words of the German military strategist Helmuth von Moltke, no battle plan survives contact with the enemy.

Here’s a fascinating real world example, sent to us by a friend in South Africa, Kokkie Kooyman.

Imagine you are a shareholder in Warren Buffett’s legendary holding company, Berkshire Hathaway. You’ve already enjoyed some fabulous returns, having tagged along on Buffett’s coattails ever since he started his first partnership in 1956.

It is now 1975.

In 1971, you had $10,000 invested in Berkshire Hathaway stock. You have a friend who had an identical amount invested in the S&P 500 stock index.

Then the Arab oil embargo happens. The oil price soars from $3 a barrel to nearly $12. The stock market collapses. Berkshire is not immune. By 1974, your Berkshire shares are worth $5,708. Your friend is doing badly, but better than you – his investment is worth $7,456.

Now, in 1975, you begin to reassess your portfolio. Your friend has bounced back into the black. His grubstake in the S&P 500 is back above $10,000. But your shares in Berkshire are now almost half of what they were worth four years ago. The stock market has recovered, but your shareholding hasn’t. Ask yourself honestly. What would you have done ?

We suspect that in 1975, most investors would have bailed on Buffett. Underperformance relative to the market for one calendar year is difficult enough to stomach. But sitting through four years of relative underperformance is a really tough ask. Not many investors, we suggest, would have had the stamina.

Selling Berkshire in 1975, of course, would have been a colossal mistake, with the benefit of hindsight. Within just a year, the value of the Berkshire holding would have been above that of the S&P 500 again, and back above the level of your friend’s portfolio. And by 1991, the scale of the subsequent outperformance would have been clear to all. But ask yourself again:

Would you have sold in ’75 ?

Buffett’s mentor, Ben Graham, nicely summarised these problems with his trademark brevity:

“Individuals who cannot master their emotions are ill-suited to profit from the investment process.”

Contrarian investing today is arguably even more of a challenge because it’s damnably difficult to trust the prices of any financial assets, anywhere. How can one invest rationally when all the benchmarks associated with sound investment principles have become hopelessly distorted by central bank stimulus – or by too many asset gatherers slavishly aping the composition of global institutional indices ?

Conventional investment theory holds that the investment journey begins with the “risk-free rate”: the market interest rate available on short term government debt of the highest quality. Investors can, in theory, choose to park their money in “riskless” bank deposits or “riskless” short term government bonds. If they have a higher appetite for risk, they should be able to earn a spread above the risk-free rate by holding bonds of inferior credit quality (corporate debt, for example) or by buying listed equity investments instead.

There are at least two problems with this theory today. One is that the market interest rate is no longer set by anything approximating to a free market. It is set by government fiat. Or more accurately, it is set by central banks, acting as agents for those same governments.

The second is that courtesy of the price distortion inherent in Quantitative Easing and overmuch index tracking, the risk-free returns once offered by government bonds have become return-free risks. An example. Last week it emerged that the Bank of England had just sold £675 million of its UK government bond holdings. The worst sale was of the 2061 Gilt which it started buying at a price of 100 and finally sold last week at a price of £23.41.

There is a third problem. “Risk-free” implies some kind of inherent creditworthiness. But in our Alice-Through-The-Looking-Glass investment world, government bonds now struggle to offer positive real yields even as the supply of government debt has never been higher. It is as if the laws of supply and demand have been utterly rescinded. In other words, the true credit quality of western government debt has never been lower – the exact opposite of what those optically low-seeming yields would suggest.

With politicians throughout the West unable or unwilling to implement the hard choices and economic restructuring required to drag their economies out of a debt-soaked deflationary mire, central bankers have chosen to fill the resultant policy vacuum. But their policy options are limited to playing games with interest rates and money. In the absence of bold political action, central banks were allowed to create ex nihilo money and used it to buy bonds. The somewhat tenuous argument in justification of QE was that it was needed to prevent deflation. Deflation must be defeated because if it becomes entrenched, it will bankrupt heavily indebted governments. There is no evidence yet that QE has been or will be successful to this reflationary end. But there is overwhelming evidence that QE ended up gravely distorting asset prices, and succeeded in driving both bond and equity markets to levels that they may well not have reached in the absence of money-printing.

Robert Shiller’s cyclically adjusted price / earnings ratio for the US stock market (or CAPE) provides a sobering perspective on US equity valuations (with the US accounting for over 70% of the MSCI World Equity Index). It offers a 10 year smoothed average of the US market’s p/e multiple.

Shiller P/E, 1880 to 2026

Source: http://www.multpl.com/shiller-pe/

As you can see from the chart, with a current multiple of over 40 times, the Shiller p/e stands at over twice its long run average of 17.4. (A caveat required here is that the Shiller p/e is not particularly useful as an aid for market timing: as the late 1990s experience shows, the stock market can remain, with hindsight, fundamentally overvalued for quite extensive periods.)

All of which makes us despair at the growing number of individuals flooding into the market indiscriminately today, by buying passive ETFs (Exchange Traded Funds), at what are close to all-time highs.

But there’s the stock market, and then there’s the market for individual stocks. While the ongoing crisis in the Middle East virtually guarantees messily high inflation if not stagflation throughout the developed world, we are finding no shortage of attractively priced listed companies in the commodities arena which stand to benefit from an increasingly broad-based commodities rally. It’s an ill wind that blows nobody any good. The question investors must ask is whether they are man enough to detach from the herd and seize the opportunities within the cave.

………….

As you may know, we also manage bespoke investment portfolios for private clients internationally. We would be delighted to help you too. Because of the current heightened market volatility we are offering a completely free financial review, with no strings attached, to see if our value-oriented approach might benefit your portfolio – with no obligation at all:

Get your Free

financial review

…………

Tim Price is co-manager of the VT Price Value Portfolio and author of ‘Investing through the Looking Glass: a rational guide to irrational financial markets’. You can access a full archive of these weekly investment commentaries here. You can listen to our regular ‘State of the Markets’ podcasts, with Paul Rodriguez of ThinkTrading.com, here. Email us: info@pricevaluepartners.com.

Price Value Partners manage investment portfolios for private clients. We also manage the VT Price Value Portfolio, an unconstrained global fund investing in Benjamin Graham-style value stocks and real assets, and also in systematic trend-following funds.

Take a closer look

Take a look at the data of our investments and see what makes us different.

LOOK CLOSERSubscribe

Sign up for the latest news on investments and market insights.

KEEP IN TOUCHContact us

In order to find out more about PVP please get in touch with our team.

CONTACT USTim Price