“The truth is rarely pure and never simple.”

- Oscar Wilde (‘The Importance of Being Earnest’).

“No matter how cynical you get, it is impossible to keep up.”

Get your Free

financial review

Shortly before he went off the reservation in service of the World Economic Forum, Yuval Noah Harari wrote a book called ‘Sapiens’. Human beings are not evolutionarily well adapted to stock markets (for example). Homo sapiens and the human brain started their evolutionary journey on the plains of Africa 300,000 years ago. Stock markets have only been with us for a couple of hundred years. Yuval Noah Harari suggests in his book that what distinguishes between homo sapiens and our other ancient contemporaries whose evolutionary lines have died out is our enthusiasm for, and adeptness at, storytelling. Whether a story is even true may be less important than just how compelling it is. Human beings also crave certainty, so we would rather buy into a false narrative than accept that the world is a deeply uncertain and unpredictable place. Which partly accounts for why financial journalism is such an intellectual backwater. Thomas Schuster of the Institute for Communication and Media Studies at Leipzig University, nails it:

“The media select, they interpret, they emotionalize and they create facts. The media not only reduce reality by lowering information density. They focus reality by accumulating information where ‘actually’ none exists. A typical stock market report looks like this: Stock X increased because… Index Y crashed due to… Prices Z continue to rise after… Most of these explanations are post-hoc rationalizations. An artificial logic is created, based on a simplistic understanding of the markets, which implies that there are simple explanations for most price movements; that price movements follow rules which then lead to systematic patterns; and of course that the news disseminated by the media decisively contribute to the emergence of price movements.”

One narrative that has only grown in strength over the past month is that the ‘chaos’ of the Trump tariffs amounts to some kind of existential threat to the economic primacy of the United States and of the US dollar. We disagree, and side with Grant Williams instead. The existential rot and the ‘looting of the Treasury’ stage of geopolitical proceedings set in under the Biden administration and its response to the invasion of Ukraine:

“This freezing of Russian central bank assets after the Ukraine invasion and the subsequent appropriation of the interest payments on that $325 billion of assets changed the calculus for every central bank in the world. Every single one of them now knows that there are a set of circumstances under which the U.S. government will confiscate your sovereign reserves, period.”

As a friend pointed out at the time (February 2022), even at the height of World War II, the BIS, the Bank for International Settlements – the so-called central bank for central banks – never dared to attack Nazi Germany’s foreign reserves. That is a sign of just how morally bankrupt (and heedless of real world ramifications) the Biden administration and the EU and their allies were in their support for Ukraine.

Grant Williams again:

“This is not a Trump thing by any means. Let’s be clear about that. We go back to Obama and the ‘08 financial crisis. Obama had the mandate and the opportunity to really stick it to wrongdoers, and he completely gave them a pass. Whether that was Hank Paulson driven, I suspect he was a big voice in that. I don’t know. But this absence of consequence is what troubles me the most because that’s how you undermine a society built on the rule of law that has been the foundation.

“Property rights, the rule of law, has been the foundation of western society. I can see it being chipped away. That’s the thing, beyond all Trump’s bluster, I can get past that easily as it turns out, because I have the ability to read pieces like yours [Barth’s] that bring me back to the reality of this, and the previous parallels and say, look, it’s happened before. The world didn’t end. There are ways through this. But I struggle to get past this denuding of the office itself. Without an office, what are we really doing here? Where do we look to for leadership, for probity, for all these things that have stood for so much for so long?”

You can listen to our own recent interview with Grant here.

Which is why the so-called ‘fundamentals’ (i.e. subjective narratives about geopolitical and economic trends) can only get you so far. Once the legacy media gets around to plastering a financial story over the front page, it is already too late to do anything profitable about it. And in a quote attributed to General George S. Patton,

“If everyone is thinking alike, then somebody isn’t thinking.”

Which is why we believe that genuine and enduring investment wealth tends to accrue to patient contrarians.

Here are some narratives that we suspect might be deadly today:

“Chief amongst these [impossible] notions are the beliefs that we can spend our way to prosperity, borrow our way to solvency, and innovate our way past material limitations demarcated by the planet’s resources and the laws of physics.

“Our specific ‘remedies’ for the ending and reversal of growth are monetary innovation and technological advance. Such propositions disregard the facts, which are that money commands value only as an exchangeable claim on the material, and that the potential scope of technology is bounded by the limits of physical possibility.

“These considerations define two of the greatest shocks that we will encounter as reality refuses to submit to the imperatives of wishful thinking.

“Bluntly stated, the financial system will crash into cascading defaults and runaway inflation, whilst technology will fail to deliver on the unrealistic expectations vested in it.

“Both of these failures are already unfolding. Debts and quasi-debts are expanding at wholly unsustainable rates, whilst the activities that we term “tech” are trapped in a relentless process of diminishing returns.”

Source: Dr. Tim Morgan, ‘At the end of modernity’, 5th May 2025.

And here is a(n unpopular) narrative that we suspect might be insanely profitable today:

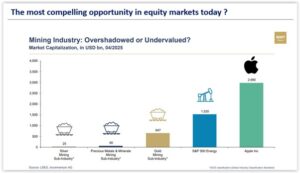

Silver is grotesquely under-owned and poised for greatness. The following graphics, courtesy of our friends at Incrementum, indicate why:

Few resources are as valuable to the modern world as silver. As the world’s most conductive metal, it is an essential input into the digital economy. It is also a core component of solar panels, wind turbines and electric vehicles. And for at least the last five years, the physical silver market has been in deficit, that is to say the world is using up more silver in industrial applications than it has managed to extract from below ground. As investors, therefore, you have a simple binary choice. You can choose to buy Apple Inc., for example. Or for the same outlay, you could buy the entire listed silver mining industry 120 times over. We believe the latter option is screaming ‘opportunity’, and our fund is positioned accordingly.

We are reminded by our friend Tony Deden that three of the most important characteristics he seeks in investments are independence, scarcity and permanence. Each of these also applies to gold, for example. Not one single one of them applies to the narratives of either politicians or the legacy media.

………….

As you may know, we also manage bespoke investment portfolios for private clients internationally. We would be delighted to help you too. Because of the current heightened market volatility we are offering a completely free financial review, with no strings attached, to see if our value-oriented approach might benefit your portfolio – with no obligation at all:

Get your Free

financial review

…………

Tim Price is co-manager of the VT Price Value Portfolio and author of ‘Investing through the Looking Glass: a rational guide to irrational financial markets’. You can access a full archive of these weekly investment commentaries here. You can listen to our regular ‘State of the Markets’ podcasts, with Paul Rodriguez of ThinkTrading.com, here. Email us: info@pricevaluepartners.com.

Price Value Partners manage investment portfolios for private clients. We also manage the VT Price Value Portfolio, an unconstrained global fund investing in Benjamin Graham-style value stocks and also in systematic trend-following funds.

“The truth is rarely pure and never simple.”

“No matter how cynical you get, it is impossible to keep up.”

Get your Free

financial review

Shortly before he went off the reservation in service of the World Economic Forum, Yuval Noah Harari wrote a book called ‘Sapiens’. Human beings are not evolutionarily well adapted to stock markets (for example). Homo sapiens and the human brain started their evolutionary journey on the plains of Africa 300,000 years ago. Stock markets have only been with us for a couple of hundred years. Yuval Noah Harari suggests in his book that what distinguishes between homo sapiens and our other ancient contemporaries whose evolutionary lines have died out is our enthusiasm for, and adeptness at, storytelling. Whether a story is even true may be less important than just how compelling it is. Human beings also crave certainty, so we would rather buy into a false narrative than accept that the world is a deeply uncertain and unpredictable place. Which partly accounts for why financial journalism is such an intellectual backwater. Thomas Schuster of the Institute for Communication and Media Studies at Leipzig University, nails it:

“The media select, they interpret, they emotionalize and they create facts. The media not only reduce reality by lowering information density. They focus reality by accumulating information where ‘actually’ none exists. A typical stock market report looks like this: Stock X increased because… Index Y crashed due to… Prices Z continue to rise after… Most of these explanations are post-hoc rationalizations. An artificial logic is created, based on a simplistic understanding of the markets, which implies that there are simple explanations for most price movements; that price movements follow rules which then lead to systematic patterns; and of course that the news disseminated by the media decisively contribute to the emergence of price movements.”

One narrative that has only grown in strength over the past month is that the ‘chaos’ of the Trump tariffs amounts to some kind of existential threat to the economic primacy of the United States and of the US dollar. We disagree, and side with Grant Williams instead. The existential rot and the ‘looting of the Treasury’ stage of geopolitical proceedings set in under the Biden administration and its response to the invasion of Ukraine:

“This freezing of Russian central bank assets after the Ukraine invasion and the subsequent appropriation of the interest payments on that $325 billion of assets changed the calculus for every central bank in the world. Every single one of them now knows that there are a set of circumstances under which the U.S. government will confiscate your sovereign reserves, period.”

As a friend pointed out at the time (February 2022), even at the height of World War II, the BIS, the Bank for International Settlements – the so-called central bank for central banks – never dared to attack Nazi Germany’s foreign reserves. That is a sign of just how morally bankrupt (and heedless of real world ramifications) the Biden administration and the EU and their allies were in their support for Ukraine.

Grant Williams again:

“This is not a Trump thing by any means. Let’s be clear about that. We go back to Obama and the ‘08 financial crisis. Obama had the mandate and the opportunity to really stick it to wrongdoers, and he completely gave them a pass. Whether that was Hank Paulson driven, I suspect he was a big voice in that. I don’t know. But this absence of consequence is what troubles me the most because that’s how you undermine a society built on the rule of law that has been the foundation.

“Property rights, the rule of law, has been the foundation of western society. I can see it being chipped away. That’s the thing, beyond all Trump’s bluster, I can get past that easily as it turns out, because I have the ability to read pieces like yours [Barth’s] that bring me back to the reality of this, and the previous parallels and say, look, it’s happened before. The world didn’t end. There are ways through this. But I struggle to get past this denuding of the office itself. Without an office, what are we really doing here? Where do we look to for leadership, for probity, for all these things that have stood for so much for so long?”

You can listen to our own recent interview with Grant here.

Which is why the so-called ‘fundamentals’ (i.e. subjective narratives about geopolitical and economic trends) can only get you so far. Once the legacy media gets around to plastering a financial story over the front page, it is already too late to do anything profitable about it. And in a quote attributed to General George S. Patton,

“If everyone is thinking alike, then somebody isn’t thinking.”

Which is why we believe that genuine and enduring investment wealth tends to accrue to patient contrarians.

Here are some narratives that we suspect might be deadly today:

“Chief amongst these [impossible] notions are the beliefs that we can spend our way to prosperity, borrow our way to solvency, and innovate our way past material limitations demarcated by the planet’s resources and the laws of physics.

“Our specific ‘remedies’ for the ending and reversal of growth are monetary innovation and technological advance. Such propositions disregard the facts, which are that money commands value only as an exchangeable claim on the material, and that the potential scope of technology is bounded by the limits of physical possibility.

“These considerations define two of the greatest shocks that we will encounter as reality refuses to submit to the imperatives of wishful thinking.

“Bluntly stated, the financial system will crash into cascading defaults and runaway inflation, whilst technology will fail to deliver on the unrealistic expectations vested in it.

“Both of these failures are already unfolding. Debts and quasi-debts are expanding at wholly unsustainable rates, whilst the activities that we term “tech” are trapped in a relentless process of diminishing returns.”

Source: Dr. Tim Morgan, ‘At the end of modernity’, 5th May 2025.

And here is a(n unpopular) narrative that we suspect might be insanely profitable today:

Silver is grotesquely under-owned and poised for greatness. The following graphics, courtesy of our friends at Incrementum, indicate why:

Few resources are as valuable to the modern world as silver. As the world’s most conductive metal, it is an essential input into the digital economy. It is also a core component of solar panels, wind turbines and electric vehicles. And for at least the last five years, the physical silver market has been in deficit, that is to say the world is using up more silver in industrial applications than it has managed to extract from below ground. As investors, therefore, you have a simple binary choice. You can choose to buy Apple Inc., for example. Or for the same outlay, you could buy the entire listed silver mining industry 120 times over. We believe the latter option is screaming ‘opportunity’, and our fund is positioned accordingly.

We are reminded by our friend Tony Deden that three of the most important characteristics he seeks in investments are independence, scarcity and permanence. Each of these also applies to gold, for example. Not one single one of them applies to the narratives of either politicians or the legacy media.

………….

As you may know, we also manage bespoke investment portfolios for private clients internationally. We would be delighted to help you too. Because of the current heightened market volatility we are offering a completely free financial review, with no strings attached, to see if our value-oriented approach might benefit your portfolio – with no obligation at all:

Get your Free

financial review

…………

Tim Price is co-manager of the VT Price Value Portfolio and author of ‘Investing through the Looking Glass: a rational guide to irrational financial markets’. You can access a full archive of these weekly investment commentaries here. You can listen to our regular ‘State of the Markets’ podcasts, with Paul Rodriguez of ThinkTrading.com, here. Email us: info@pricevaluepartners.com.

Price Value Partners manage investment portfolios for private clients. We also manage the VT Price Value Portfolio, an unconstrained global fund investing in Benjamin Graham-style value stocks and also in systematic trend-following funds.

Take a closer look

Take a look at the data of our investments and see what makes us different.

LOOK CLOSERSubscribe

Sign up for the latest news on investments and market insights.

KEEP IN TOUCHContact us

In order to find out more about PVP please get in touch with our team.

CONTACT USTim Price