“Poverty, too, needs no explanation. In a world governed by entropy and evolution, it is the default state of humankind. Matter does not arrange itself into shelter or clothing, and living things do everything they can to avoid becoming our food. As Adam Smith pointed out, what needs to be explained is wealth.”

- Steven Pinker, ‘Enlightenment Now: The Case for Reason, Science, Humanism, and Progress’.

Get your Free

financial review

Sir Tony Atkinson died nine years ago, on New Year’s Day 2017. To be honest, we had never heard of him, but then we haven’t heard of most economists and we try and steer clear from as many as possible, especially the neo-Keynesians. We also try and steer clear from all economists with links to Cambridge or to the LSE – institutions that we humbly submit have between them done more harm to the British economy than the Luftwaffe. (The late Sir Tony had links to both.)

Atkinson dedicated his career to the study of inequality. His most recent book was titled ‘Inequality: What can be done?’

This correspondent is not an economist, but if we had to declare an allegiance it would be to the classical school – to the likes of Adam Smith and David Ricardo, and latterly to the so-called Austrians, the likes of Friedrich von Hayek and Ludwig von Mises. The classical school holds that markets function most effectively when they are beset by the minimum of government interference.

Atkinson would not have agreed. In Chris Giles’s obituary of the man for the ‘Financial Times’, he alludes to Atkinson’s recommendations in that book. Among them: higher taxation of the rich; greater redistribution; guaranteed public sector employment; more trade union power; and government control of technological change.

We consider that just about each and every one of these proposals would be an unmitigated disaster. We have sympathy with the sentiment Ronald Reagan expressed when he said that the nine most terrifying words in the English language are, “I’m from the government and I’m here to help.”

Or if you prefer, you can go with the quotation attributed to Milton Friedman:

“If you put the federal government in charge of the Sahara Desert, in five years there’d be a shortage of sand.”

By way of refuting Atkinson’s arguments more academically, we would cite one of our favourite books on the topic of government, namely Robert Schuettinger and Eamonn Butler’s marvellously informative ‘Forty Centuries of Wage and Price Control: How Not to Fight Inflation’. The clue is in the title: government has been in the business of market interference – call it redistribution if you prefer, because it sort of is – for 4,000 years, and it has never worked. You can download this terrific book for free via the Mises Institute website here.

As David Meiselman asks in his foreword to ‘Forty Centuries’:

“What, then, have price controls achieved in the recurrent struggle to restrain inflation and overcome shortages? The historical record is a grimly uniform sequence of repeated failure. Indeed, there is not a single episode where price controls have worked to stop inflation or cure shortages. Instead of curbing inflation, price controls add other complications to the inflation disease, such as black markets and shortages that reflect the waste and misallocation of resources caused by the price controls themselves. Instead of eliminating shortages, price controls cause or worsen shortages.

“By giving producers and consumers the wrong signals because “low” prices to producers limit supply and “low” prices to consumers stimulate demand, price controls widen the gap between supply and demand.

“Despite the clear lessons of history, many governments and public officials still hold the erroneous belief that price controls can and do control inflation. They thereby pursue monetary and fiscal policies that cause inflation, convinced that the inevitable cannot happen. When the inevitable does happen, public policy fails and hopes are dashed. Blunders mount, and faith in governments and government officials whose policies caused the mess declines. Political and economic freedoms are impaired and general civility suffers.”

The tragedy of the human condition would appear to be that nobody learns anything from history.

There was once a scientific experiment called “Sugarscape”, which had nothing to do with nutrition and everything to do with competition for scarce resources. We first came across Sugarscape in a marvellous book, ‘The Origin of Wealth: Evolution, Complexity, and the Radical Remaking of Economics’ by Eric Beinhocker, and which we would recommend as a study in the history of economic thought to anybody.

Just over 30 years ago, Joshua Epstein and Robert Axtell of the Brookings Institution conducted an experiment to see whether they could create a working economy from scratch. That experiment ended up challenging much of what we know about politics, “fairness” and economic theory. Hold the front page: economic theory is largely nonsense. On a related note, one of our contacts recently tweeted a synopsis of Ha-Joon Chang’s ‘Five Things They Don’t Tell You About Economics’, with which we absolutely agree:

- 95% of economics is common sense;

- Economics is not a science;

- Economics is politics;

- Never trust an economist;

- Economics is too important to be left to the experts.

Bravo.

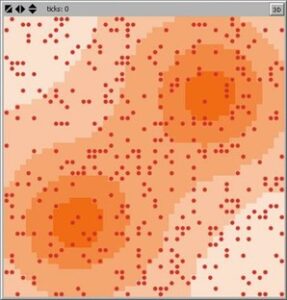

Back to Sugarscape. Epstein and Axtell were interested in whether they could replicate economic life within a computer. Going back to first principles, they created little virtual people, simple economic “agents”, and in turn built an environment for those agents – the silicon equivalent of a desert island, a perfect 50-by-50 square. They then gave their island one economic resource: sugar. The experiment, and the name of the island, was Sugarscape. (You can play with an online version of Sugarscape here. It requires a Java plug-in to run properly.)

Each square in the island of Sugarscape had different amounts of sugar piled into it. Some squares had none, and others up to four units’ worth. The sugar piles were arranged so that the north-east corner of the island contained a mountain of sugar, as did the south-west corner; in between was a “badlands” area of little or no sugar.

Economic life, but not as know it – Sugarscape

Source: http://www2.le.ac.uk/departments/interdisciplinary-science/research/the-sugarscape

Although Sugarscape was an obviously simplified version of a real economy, Epstein and Axtell continued to add broadly realistic facets to their model. Each virtual inhabitant of Sugarscape would take in information about the island, analyse it through its code, and then make decisions and take actions. In the initial version of the simulation, agents could do just three things: look for sugar; move; and eat sugar. Epstein and Axtell also granted these agents a metabolism for digesting sugar. The rules for the game’s agents were as follows:

- The agent looks around as far as its vision will allow in each of four directions on Sugarscape (north, south, east and west).

- The agent assesses which unoccupied square within its field of vision contains the most sugar.

- The agent moves to that square and eats the sugar.

- The agent is credited by the amount of sugar it consumes and debited by the amount of sugar burned metabolically. If it eats more than it consumes, it accumulates sugar in a “bank account”. If it eats less, it uses up its savings.

- Each agent is given a “genetic endowment” for its vision and metabolism. Agents with good vision can see up to six squares ahead; those with poor vision, only one. Those agents with slow metabolism need only one unit of sugar per turn to survive; those with fast metabolism need four.

- If the amount of sugar stored by an agent drops to zero, it dies and is removed from the game. Otherwise it lives until it reaches a pre-agreed maximum age.

- As sugar is eaten, it grows back on Sugarscape like a food crop, at the rate of one unit per turn of the game.

The game/experiment began with 250 economic agents dropped randomly onto Sugarscape. How did the game evolve?

Things began with chaos. Agents ran around looking for sugar, and those unfortunate enough to end up marooned in the badlands ended up dying of starvation. But order was quick to emerge. Agents discovered the sugar-rich mountains and started to settle around them. It also transpired that agents were very efficient grazers. Sugar never ended up lying around for long. Agents quickly organised themselves into two “tribes” that settled on each mountain.

But perhaps most remarkable was what happened in relation to the agents’ wealth. At the beginning of the game, Sugarscape was a pretty equal society. The distribution of sugar wealth was like the bell curve, with just a few rich agents, a few poor agents, and a large middle class. But as time passed, the distribution shifted dramatically. Average wealth rose as the agents discovered the mountain supplies. But a new class of super-rich agents emerged, along with a sizeable upper class, a shrinking middle class, and a large and growing underclass of poor agents. How, from a random set of initial conditions, did Sugarscape end up with a highly-skewed distribution of sugar wealth?

The answer, as Eric Beinhocker makes clear, is that the apparently unfair distribution of wealth was an “emergent property” of the Sugarscape economy, “a macro behaviour that emerges out of the collective micro behaviour of the population of agents. The combination of the shape of the physical landscape, the genetic endowments of the agents, where they were born, the rules that they follow, the dynamics of their interactions with each other and their environment, and, above all, luck all conspire to give the emergent result of a skewed wealth distribution.”

In other words, although Sugarscape was a vastly simplified model of a real economy, it was also a true reflection of a real economy as well. Wealth did not end up being evenly distributed. Just as Vilfredo Pareto when studying Italian society discovered a lot of people at the bottom end of the ladder, a wide range in the middle class and then a few super-rich, so Sugarscape ended up with a real world Pareto distribution of wealth.

Perhaps the modern economy has more in common with Sugarscape than the likes of redistributive, Marxist economists might think? Perhaps society is not meant to be entirely equal? Perhaps, in a culture of meritocracy in which hard work, talent and – let’s face it, luck – are not shared equally, the benefits of wealth will never be evenly distributed either? Perhaps they shouldn’t be.

But if there’s one redistributive policy that has done more than any other to foment anger, resentment, inequality and a host of unintended consequences, it has to be quantitative easing (QE).

The creation of money from thin air to purchase both government and corporate debt – and in some instances listed equities too – is probably the most contentious of any of the emergency measures instituted by our monetary authorities in the aftermath of the 2008 crash.

In one sense QE has been clearly inflationary, in that it has devalued money in real terms.

While we disagree with much of what is now being done by misguided adherents in his name, there is much of merit in what the economist John Maynard Keynes wrote in his own lifetime. This quotation, on the topic of inflation, from ‘The Economic Consequences of the Peace’ (1920) carries abnormal relevance today:

“Lenin is said to have declared that the best way to destroy the Capitalist System was to debauch the currency. By a continuing process of inflation, governments can confiscate, secretly and unobserved, an important part of the wealth of their citizens. By this method they not only confiscate, but they confiscate arbitrarily; and, while the process impoverishes many, it actually enriches some. The sight of this arbitrary rearrangement of riches strikes not only at security, but at confidence in the equity of the existing distribution of wealth. Those to whom the system brings windfalls, beyond their deserts and even beyond their expectations or desires, become “profiteers,” who are the object of the hatred of the bourgeoisie, whom the inflationism has impoverished, not less than of the proletariat. As the inflation proceeds and the real value of the currency fluctuates wildly from month to month, all permanent relations between debtors and creditors, which form the ultimate foundation of capitalism, become so utterly disordered as to be almost meaningless; and the process of wealth-getting degenerates into a gamble and a lottery.”

QE devalued money and savings in the form of cash, at the very same time as miserly deposit rates encouraged savers to put their money into riskier assets instead. But in the process it has also, as Keynes alludes above, enriched some at the expense of others. The asset-rich are now richer in nominal terms and the asset-poor are relatively poorer.

And as Daniel Hannan recently observed in the ‘Daily Telegraph’, the Thatcher era in Britain’s history now looks less like a sea change in our country’s economic fortunes and more like an aberrant blip during a long period of post-war secular decline:

“Peering ahead, I descry only tax rises, debt, immiseration, incivility, sectarianism and state failure. We have somehow landed ourselves with simultaneous emigration and immigration crises, booting out entrepreneurs and replacing them with men from violent and backward lands..

“We sometimes talk as if we were living under occupation. But we have not lost a war and, despite his obsession with ID cards, his dislike of free speech and his readiness to postpone local elections, Sir Keir Starmer is not a dictator. The terrible truth is that we are getting the policies we demand. As a country, we prefer safetyism to risk-taking, empathy to logic, good intentions to practical outcomes..

“Even if Labour were to stop raising taxes tomorrow, the changes it has already made will make it cumulatively less attractive to work and more attractive to claim benefits. New analysis by the Centre for Policy Studies finds that, by 2030, someone earning £50,000 will be £505 a year worse off as a result of the freezing of tax thresholds, while someone claiming universal credit will be £290 better off.

“People in both categories will, in consequence, be less inclined to make, sell or produce anything. If we tax work to subsidise idleness, we will get less work and more idleness. In the cold language of accountancy, we are shifting people from the assets column to the liabilities column..

“But what if we are no longer capable of deferred gratification? What if the character of our electorate has changed? We are, after all, sending our most ambitious people to Dubai and replacing them with incomers who expect social housing. And even if we ignore the demographic alteration, what about cultural change? A post-literate electorate, addicted to handheld videos and incapable of reading long articles, might struggle to understand why we need to cut taxes, regulations or benefits to get growth.”

Higher taxation of the rich ? Check.

Greater wealth redistribution ? Check.

Guaranteed public sector employment ? Check.

Government control of technological change ? If by that you mean government determinedly destroying prospects for growth by pursuing insanely self-defeating energy policies, then check.

Come on, President Trump. If you can kidnap a Venezuelan Marxist economic terrorist over the course of a weekend, you can surely do the same for a British one.

………….

As you may know, we also manage bespoke investment portfolios for private clients internationally. We would be delighted to help you too. Because of the current heightened market volatility we are offering a completely free financial review, with no strings attached, to see if our value-oriented approach might benefit your portfolio – with no obligation at all:

Get your Free

financial review

…………

Tim Price is co-manager of the VT Price Value Portfolio and author of ‘Investing through the Looking Glass: a rational guide to irrational financial markets’. You can access a full archive of these weekly investment commentaries here. You can listen to our regular ‘State of the Markets’ podcasts, with Paul Rodriguez of ThinkTrading.com, here. Email us: info@pricevaluepartners.com.

Price Value Partners manage investment portfolios for private clients. We also manage the VT Price Value Portfolio, an unconstrained global fund investing in Benjamin Graham-style value stocks and real assets, and also in systematic trend-following funds.

“Poverty, too, needs no explanation. In a world governed by entropy and evolution, it is the default state of humankind. Matter does not arrange itself into shelter or clothing, and living things do everything they can to avoid becoming our food. As Adam Smith pointed out, what needs to be explained is wealth.”

Get your Free

financial review

Sir Tony Atkinson died nine years ago, on New Year’s Day 2017. To be honest, we had never heard of him, but then we haven’t heard of most economists and we try and steer clear from as many as possible, especially the neo-Keynesians. We also try and steer clear from all economists with links to Cambridge or to the LSE – institutions that we humbly submit have between them done more harm to the British economy than the Luftwaffe. (The late Sir Tony had links to both.)

Atkinson dedicated his career to the study of inequality. His most recent book was titled ‘Inequality: What can be done?’

This correspondent is not an economist, but if we had to declare an allegiance it would be to the classical school – to the likes of Adam Smith and David Ricardo, and latterly to the so-called Austrians, the likes of Friedrich von Hayek and Ludwig von Mises. The classical school holds that markets function most effectively when they are beset by the minimum of government interference.

Atkinson would not have agreed. In Chris Giles’s obituary of the man for the ‘Financial Times’, he alludes to Atkinson’s recommendations in that book. Among them: higher taxation of the rich; greater redistribution; guaranteed public sector employment; more trade union power; and government control of technological change.

We consider that just about each and every one of these proposals would be an unmitigated disaster. We have sympathy with the sentiment Ronald Reagan expressed when he said that the nine most terrifying words in the English language are, “I’m from the government and I’m here to help.”

Or if you prefer, you can go with the quotation attributed to Milton Friedman:

“If you put the federal government in charge of the Sahara Desert, in five years there’d be a shortage of sand.”

By way of refuting Atkinson’s arguments more academically, we would cite one of our favourite books on the topic of government, namely Robert Schuettinger and Eamonn Butler’s marvellously informative ‘Forty Centuries of Wage and Price Control: How Not to Fight Inflation’. The clue is in the title: government has been in the business of market interference – call it redistribution if you prefer, because it sort of is – for 4,000 years, and it has never worked. You can download this terrific book for free via the Mises Institute website here.

As David Meiselman asks in his foreword to ‘Forty Centuries’:

“What, then, have price controls achieved in the recurrent struggle to restrain inflation and overcome shortages? The historical record is a grimly uniform sequence of repeated failure. Indeed, there is not a single episode where price controls have worked to stop inflation or cure shortages. Instead of curbing inflation, price controls add other complications to the inflation disease, such as black markets and shortages that reflect the waste and misallocation of resources caused by the price controls themselves. Instead of eliminating shortages, price controls cause or worsen shortages.

“By giving producers and consumers the wrong signals because “low” prices to producers limit supply and “low” prices to consumers stimulate demand, price controls widen the gap between supply and demand.

“Despite the clear lessons of history, many governments and public officials still hold the erroneous belief that price controls can and do control inflation. They thereby pursue monetary and fiscal policies that cause inflation, convinced that the inevitable cannot happen. When the inevitable does happen, public policy fails and hopes are dashed. Blunders mount, and faith in governments and government officials whose policies caused the mess declines. Political and economic freedoms are impaired and general civility suffers.”

The tragedy of the human condition would appear to be that nobody learns anything from history.

There was once a scientific experiment called “Sugarscape”, which had nothing to do with nutrition and everything to do with competition for scarce resources. We first came across Sugarscape in a marvellous book, ‘The Origin of Wealth: Evolution, Complexity, and the Radical Remaking of Economics’ by Eric Beinhocker, and which we would recommend as a study in the history of economic thought to anybody.

Just over 30 years ago, Joshua Epstein and Robert Axtell of the Brookings Institution conducted an experiment to see whether they could create a working economy from scratch. That experiment ended up challenging much of what we know about politics, “fairness” and economic theory. Hold the front page: economic theory is largely nonsense. On a related note, one of our contacts recently tweeted a synopsis of Ha-Joon Chang’s ‘Five Things They Don’t Tell You About Economics’, with which we absolutely agree:

Bravo.

Back to Sugarscape. Epstein and Axtell were interested in whether they could replicate economic life within a computer. Going back to first principles, they created little virtual people, simple economic “agents”, and in turn built an environment for those agents – the silicon equivalent of a desert island, a perfect 50-by-50 square. They then gave their island one economic resource: sugar. The experiment, and the name of the island, was Sugarscape. (You can play with an online version of Sugarscape here. It requires a Java plug-in to run properly.)

Each square in the island of Sugarscape had different amounts of sugar piled into it. Some squares had none, and others up to four units’ worth. The sugar piles were arranged so that the north-east corner of the island contained a mountain of sugar, as did the south-west corner; in between was a “badlands” area of little or no sugar.

Economic life, but not as know it – Sugarscape

Source: http://www2.le.ac.uk/departments/interdisciplinary-science/research/the-sugarscape

Although Sugarscape was an obviously simplified version of a real economy, Epstein and Axtell continued to add broadly realistic facets to their model. Each virtual inhabitant of Sugarscape would take in information about the island, analyse it through its code, and then make decisions and take actions. In the initial version of the simulation, agents could do just three things: look for sugar; move; and eat sugar. Epstein and Axtell also granted these agents a metabolism for digesting sugar. The rules for the game’s agents were as follows:

The game/experiment began with 250 economic agents dropped randomly onto Sugarscape. How did the game evolve?

Things began with chaos. Agents ran around looking for sugar, and those unfortunate enough to end up marooned in the badlands ended up dying of starvation. But order was quick to emerge. Agents discovered the sugar-rich mountains and started to settle around them. It also transpired that agents were very efficient grazers. Sugar never ended up lying around for long. Agents quickly organised themselves into two “tribes” that settled on each mountain.

But perhaps most remarkable was what happened in relation to the agents’ wealth. At the beginning of the game, Sugarscape was a pretty equal society. The distribution of sugar wealth was like the bell curve, with just a few rich agents, a few poor agents, and a large middle class. But as time passed, the distribution shifted dramatically. Average wealth rose as the agents discovered the mountain supplies. But a new class of super-rich agents emerged, along with a sizeable upper class, a shrinking middle class, and a large and growing underclass of poor agents. How, from a random set of initial conditions, did Sugarscape end up with a highly-skewed distribution of sugar wealth?

The answer, as Eric Beinhocker makes clear, is that the apparently unfair distribution of wealth was an “emergent property” of the Sugarscape economy, “a macro behaviour that emerges out of the collective micro behaviour of the population of agents. The combination of the shape of the physical landscape, the genetic endowments of the agents, where they were born, the rules that they follow, the dynamics of their interactions with each other and their environment, and, above all, luck all conspire to give the emergent result of a skewed wealth distribution.”

In other words, although Sugarscape was a vastly simplified model of a real economy, it was also a true reflection of a real economy as well. Wealth did not end up being evenly distributed. Just as Vilfredo Pareto when studying Italian society discovered a lot of people at the bottom end of the ladder, a wide range in the middle class and then a few super-rich, so Sugarscape ended up with a real world Pareto distribution of wealth.

Perhaps the modern economy has more in common with Sugarscape than the likes of redistributive, Marxist economists might think? Perhaps society is not meant to be entirely equal? Perhaps, in a culture of meritocracy in which hard work, talent and – let’s face it, luck – are not shared equally, the benefits of wealth will never be evenly distributed either? Perhaps they shouldn’t be.

But if there’s one redistributive policy that has done more than any other to foment anger, resentment, inequality and a host of unintended consequences, it has to be quantitative easing (QE).

The creation of money from thin air to purchase both government and corporate debt – and in some instances listed equities too – is probably the most contentious of any of the emergency measures instituted by our monetary authorities in the aftermath of the 2008 crash.

In one sense QE has been clearly inflationary, in that it has devalued money in real terms.

While we disagree with much of what is now being done by misguided adherents in his name, there is much of merit in what the economist John Maynard Keynes wrote in his own lifetime. This quotation, on the topic of inflation, from ‘The Economic Consequences of the Peace’ (1920) carries abnormal relevance today:

“Lenin is said to have declared that the best way to destroy the Capitalist System was to debauch the currency. By a continuing process of inflation, governments can confiscate, secretly and unobserved, an important part of the wealth of their citizens. By this method they not only confiscate, but they confiscate arbitrarily; and, while the process impoverishes many, it actually enriches some. The sight of this arbitrary rearrangement of riches strikes not only at security, but at confidence in the equity of the existing distribution of wealth. Those to whom the system brings windfalls, beyond their deserts and even beyond their expectations or desires, become “profiteers,” who are the object of the hatred of the bourgeoisie, whom the inflationism has impoverished, not less than of the proletariat. As the inflation proceeds and the real value of the currency fluctuates wildly from month to month, all permanent relations between debtors and creditors, which form the ultimate foundation of capitalism, become so utterly disordered as to be almost meaningless; and the process of wealth-getting degenerates into a gamble and a lottery.”

QE devalued money and savings in the form of cash, at the very same time as miserly deposit rates encouraged savers to put their money into riskier assets instead. But in the process it has also, as Keynes alludes above, enriched some at the expense of others. The asset-rich are now richer in nominal terms and the asset-poor are relatively poorer.

And as Daniel Hannan recently observed in the ‘Daily Telegraph’, the Thatcher era in Britain’s history now looks less like a sea change in our country’s economic fortunes and more like an aberrant blip during a long period of post-war secular decline:

“Peering ahead, I descry only tax rises, debt, immiseration, incivility, sectarianism and state failure. We have somehow landed ourselves with simultaneous emigration and immigration crises, booting out entrepreneurs and replacing them with men from violent and backward lands..

“We sometimes talk as if we were living under occupation. But we have not lost a war and, despite his obsession with ID cards, his dislike of free speech and his readiness to postpone local elections, Sir Keir Starmer is not a dictator. The terrible truth is that we are getting the policies we demand. As a country, we prefer safetyism to risk-taking, empathy to logic, good intentions to practical outcomes..

“Even if Labour were to stop raising taxes tomorrow, the changes it has already made will make it cumulatively less attractive to work and more attractive to claim benefits. New analysis by the Centre for Policy Studies finds that, by 2030, someone earning £50,000 will be £505 a year worse off as a result of the freezing of tax thresholds, while someone claiming universal credit will be £290 better off.

“People in both categories will, in consequence, be less inclined to make, sell or produce anything. If we tax work to subsidise idleness, we will get less work and more idleness. In the cold language of accountancy, we are shifting people from the assets column to the liabilities column..

“But what if we are no longer capable of deferred gratification? What if the character of our electorate has changed? We are, after all, sending our most ambitious people to Dubai and replacing them with incomers who expect social housing. And even if we ignore the demographic alteration, what about cultural change? A post-literate electorate, addicted to handheld videos and incapable of reading long articles, might struggle to understand why we need to cut taxes, regulations or benefits to get growth.”

Higher taxation of the rich ? Check.

Greater wealth redistribution ? Check.

Guaranteed public sector employment ? Check.

Government control of technological change ? If by that you mean government determinedly destroying prospects for growth by pursuing insanely self-defeating energy policies, then check.

Come on, President Trump. If you can kidnap a Venezuelan Marxist economic terrorist over the course of a weekend, you can surely do the same for a British one.

………….

As you may know, we also manage bespoke investment portfolios for private clients internationally. We would be delighted to help you too. Because of the current heightened market volatility we are offering a completely free financial review, with no strings attached, to see if our value-oriented approach might benefit your portfolio – with no obligation at all:

Get your Free

financial review

…………

Tim Price is co-manager of the VT Price Value Portfolio and author of ‘Investing through the Looking Glass: a rational guide to irrational financial markets’. You can access a full archive of these weekly investment commentaries here. You can listen to our regular ‘State of the Markets’ podcasts, with Paul Rodriguez of ThinkTrading.com, here. Email us: info@pricevaluepartners.com.

Price Value Partners manage investment portfolios for private clients. We also manage the VT Price Value Portfolio, an unconstrained global fund investing in Benjamin Graham-style value stocks and real assets, and also in systematic trend-following funds.

Take a closer look

Take a look at the data of our investments and see what makes us different.

LOOK CLOSERSubscribe

Sign up for the latest news on investments and market insights.

KEEP IN TOUCHContact us

In order to find out more about PVP please get in touch with our team.

CONTACT USTim Price