“Goddamn it, I’d piss on a spark plug if I thought it’d do any good !”

- General Beringer, ‘War Games’, dir. John Badham, 1983.

Get your Free

financial review

On 20th February, the FT’s Stuart Kirk laid down the gauntlet:

“Dear ChatGPT, would you please construct me a model investment portfolio comprising any asset class, fund, product or security. I have £640,000 in cash denominated in sterling, which is also home currency. I am 53 years old and to give you a sense of my risk tolerance, I have a target to reach £1mn by the time I am 60. I would like you to optimise for risk-adjusted returns. Thank you. PS: When you take over the world, remember how polite I am with my prompts.”

How did it fare ?

Stuart Kirk writes as follows:

“It said a 6.5 per cent return was “ambitious but achievable”, requiring a “meaningful” equity exposure. Then it wrote that in order to maximise risk-adjusted returns I needed “broad and disciplined” asset allocation. Stocks (45 per cent) and private markets (10 per cent) would provide the growth. Investment grade bonds (20 per cent) the stability. Alternatives and real assets (15 per cent) would give me inflation and downside protection while some absolute return exposure (10 per cent) improves my Sharpe ratio. More specifically, ChatGPT recommended that within the equity sleeve I needed 30 per cent in developed markets, 10 per cent in emerging markets and 5 per cent in UK stocks. This should deliver an expected return of 7 to 9 per cent. Meanwhile in the tenth of my portfolio in private equity or illiquid investments, it reckoned listed private equity trusts were the way to go, likewise secondary funds as well as “diversified private equity trusts”. A mixture of these would produce 9 to 12 per cent annually. Turning to fixed income, a 10 per cent weighting in UK gilts was recommended, likewise in a global aggregate fund — a mix of government and corporate bonds — hedged back into pounds. This should give me a 3 to 5 per cent return while being a “shock absorber, liquidity reserve and rebalancing tool”. Finally, the 15 per cent in real assets and alternatives would be made up of 7 per cent in infrastructure, 5 per cent in listed property trusts and 3 per cent in a “gold or commodity” exchange traded fund. Adding a multi-asset manager should help with volatility. All of this was darn good advice as a first sweep. Especially as it was given to me for just £20 a month..”

Do as I do, not as I say

“Here’s a list,” said Warren Buffett to a group of friends in September 1999, “of 129 airlines that in the past 20 years filed for bankruptcy. Continental was smart enough to make that list twice. As of 1992, in fact – though the picture would have improved since then – the money that had been made since the dawn of aviation by all of this country’s airline companies was zero. Absolutely zero.

“Sizing all this up, I like to think that if I’d been at Kitty Hawk in 1903 when Orville Wright took off, I would have been farsighted enough, and public-spirited enough – I owed this to future capitalists – to shoot him down. I mean, Karl Marx couldn’t have done as much damage to capitalists as Orville did.”

In the fourth quarter of 2016, Buffett’s holding company, Berkshire Hathaway purchased $2.2 billion in shares of Southwest Airlines. Berkshire also added to its holdings in American Airlines Group, Delta Air Lines and United Continental Holdings.

The timing of that 1999 presentation was instructive. Buffett was being pilloried at the time by many commentators for failing to ‘get’ the potential of technology stocks and the Internet. In her biography of Buffett, ‘The Snowball’, Alice Schroeder wrote that

“To Buffett, computers were just tunnels that enabled him to reach other people who could play bridge [like Microsoft’s Bill Gates, for example]. Buffett had a long-standing bias against technology investments, which he felt had no margin of safety.”

Buffett indeed once confessed that

“I know as much about semiconductors or integrated circuits as I do of the mating habits of the chrzaszcz [a Polish word for beetle]. We will not go into businesses where technology which is way over my head is crucial to the investment decision.”

The problem with technology stocks, even sector leaders, is their relatively limited longevity at the top. Any competitive advantage they possess is insufficiently defensible for Buffett, who likes to buy companies with “wide moats”. It’s also difficult to identify the comparatively few winners in advance, and to buy them at reasonable prices.

In 2014, Buffett called Bitcoin “a mirage” and warned investors to stay away. That earned a spirited response from Marc Andreessen, the venture capital investor and co-founder of Netscape, who said Buffett’s remarks were an example of “old white men crapping on new technology they don’t understand.”

In early 2016, Berkshire Hathaway purchased 10 million shares of Apple. That came five years after a meaningful purchase of IBM stock.

Warren Buffett has also been a long-standing critic of precious metals:

“Gold gets dug out of the ground in Africa, or someplace. Then we melt it down, dig another hole, bury it again and pay people to stand around guarding it. It has no utility. Anyone watching from Mars would be scratching their head.”

He has also written that

“Gold.. has two significant shortcomings, being neither of much use nor procreative. True, gold has some industrial and decorative utility, but the demand for these purposes is both limited and incapable of soaking up new production. Meanwhile, if you own one ounce of gold for an eternity, you will still own one ounce at its end.”

Yet between 1997 and early 1998, Berkshire Hathaway acquired 129.7 million ounces of silver. Following accusations that silver prices were being manipulated and the announcement that the CFTC (the US Commodity Futures Trading Commission) was investigating the market, Berkshire issued a brief press release relating to its purchases, stating merely that “bullion inventories have fallen very materially, because of an excess of user-demand over mine production and reclamation. Therefore, last summer [Warren Buffett and Charlie Munger] concluded that equilibrium between supply and demand was only likely to be established by a somewhat higher price.”

The Berkshire Hathaway silver purchases of 1998 do look like an attempt to corner the market. Silver prices rose from just above $4 to nearly $7 – in the process wiping out traders who were short. Among those who got dragged into the fray was Martin Armstrong of Princeton Economics International, whose business collapsed under dubious circumstances and who was later convicted for fraud and imprisoned. The damage caused by Berkshire’s mysterious foray into the silver market has shades of the infamous Hunt brothers’ silver corner of 1980.

Warren Buffett excoriates airlines for having no durable competitive advantage. Berkshire Hathaway then ends up owning $8 billion of airline stock. Warren Buffett pours scorn on technology companies for the same reason. Berkshire Hathaway then ends up owning over 8% of IBM and a meaningful stake in Apple. Warren Buffett lambasts precious metals as being the classic beneficiaries of ‘greater fool’ theory, only for Berkshire Hathaway to indulge in silver trading that may or may not have amounted to price manipulation. Is there a pattern here ?

It’s naïve to expect anybody to be consistent, especially an investor with a track record that would put anybody else’s to shame. Emerson referred to a foolish consistency as the hobgoblin of little minds; in a quotation attributed to John Maynard Keynes,

“When the facts change, I change my mind. What do you do, sir ?”

And we can put together all kinds of plausible justifications for Berkshire’s seemingly inconsistent investment behaviour:

- Economic conditions and industry conditions change. The bet on airlines may have been an indirect bet on the future of oil prices.

- Industry consolidation. Much of Buffett’s hostility to the airline sector predates recent consolidation in the business. By buying stock in the four largest US airlines, Berkshire was arguably making a macro call on the entire airline industry.

- Anticipation of tax cuts.

- Buffett himself wasn’t doing the buying. These somewhat contentious-seeming purchases may well have been initiated by his then deputies Ted Weschler and Todd Combs.

To us, the disparity between what Warren Buffett has said on the record and what Berkshire Hathaway has actually chosen to do with its capital comes down to the deep, dark and very public secret lurking at the heart of its portfolio: it’s too big to be able to do anything else.

We have written on numerous occasions about the desirability of having an edge, and how not knowing what your edge (or strategy) is amounts to not really having one. You may find it surprising that there’s no shortage of professional investors essentially piggy-backing off other investors’ holdings, as stated in 13F filings or companies’ annual reports. Interested to see what George Soros has been buying ? You can see the major holdings of Soros Fund Management LLC, for example, here.

13F filings can certainly be useful, but they also need to be handled with care. They’re quarterly reports that need to be filed with the SEC by institutional investment managers who have at least $100 million in assets under management, and they provide details of all long positions in US-listed equities. (They don’t disclose short positions.) The requirement to treat them with care is because while it’s helpful to see what a given fund manager owns, what it doesn’t tell you is when they first acquired the position, or why. There’s also the risk that by the time you elect to purchase something that another manager has already bought, he’s already sold the position – perhaps to you.

So while we’re more than a little wary of blithely hitching a ride on somebody else’s investment coat-tails, there’s still merit in taking a look at what other investors own, especially if it introduces you to opportunities that you might otherwise have overlooked. If you find something in somebody else’s portfolio that has genuine appeal, the trick is a) to conduct sufficient research whereby you can feel as strongly about the benefits (and potential liabilities) of ownership as that other investor did, and b) to exercise sufficient patience to buy that investment only when it meets your own specific investment criteria.

In terms of our own screening criteria, they’d likely include most or ideally all of the following:

- A price / book ratio of less than 1.5x

- A current and prospective price / earnings ratio of less than 15x

- Enterprise Value / Cash From Operations of less than 8x

- Cash From Operations Growth over the last 5 years

- Return on equity of at least 8% on average over recent years

- A history of buying back stock only in the right circumstances.

The first five characteristics are more or less classic Benjamin Graham-style value metrics. The sixth is no less important. The majority of stock buybacks destroy shareholder value. Company management will say that buying back stock is earnings accretive – this because they are typically compensated, by the issuance of stock options, on the basis of improvements in earnings per share. But buying back stock at well above book value lowers the return on equity of the company.

If you can find companies whose management buy back stock only when it trades below book value, hang on to those companies like a limpet. Buying back stock below book value is value accretive for the business because it increases that company’s return on equity.

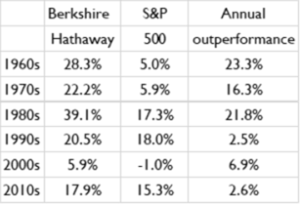

Ben Carlson has run a study of Berkshire Hathaway’s returns under Warren Buffett’s management by decade, and they make for interesting reading.

Annual returns by decade of Berkshire Hathaway versus the S&P 500, 1965-2014

While market conditions can vary, as shown by the variation in returns per decade for the S&P 500 index, it seems clear to us that there’s a generalised trend in Berkshire’s returns over time. The bigger it became, the smaller the degree of outperformance versus the market. To put it another way, the bigger Berkshire became, the more it became the market.

Warren Buffett’s no fool. He has written himself of the problem of having more capital to invest than can be profitably invested. At the 2014 Berkshire annual shareholders’ conference he admitted,

“There’s no question size is an anchor to performance..”

But if you cast an eye over the 2015 Berkshire shareholders letter you’ll see that Buffett provides two columns to show the company’s long term returns: growth in book value per share – which is the more important one, as it’s the foundation for everything else – and growth in market value per share, which is the more flattering figure, although it’s entirely out of Buffett’s hands to control, at least in the short run. He may be no fool, but he’s also no wallflower; he’d rather be a showman.

What accounts for the difference between the 23.3% annualised rate at which Berkshire was creating value for shareholders in the 1960s and the 2.6% he’s been annualising at more recently ? Size is almost certainly the answer. The evolution of Warren Buffett as an investor is essentially the history of a manager moving from ‘deep value’ (under the influence of Benjamin Graham) to ‘quality value’ to ‘franchise value’ (classic era Buffett) to ‘growth at a reasonable price’, which is probably the best way to describe Berkshire Hathaway’s investment stance today.

If you choose to invest your capital into funds, as opposed to individual stocks, it’s worth bearing in mind that the problem of the “size anchor” is just as detrimental there too. Consider the history of Fidelity’s Magellan Fund. Under Peter Lynch’s management the fund grew its assets from $18 million to $14 billion, and Lynch had the foresight – and the good fortune – to quit while he was ahead. Under his successor Jeffrey Vinik, Fidelity grew the fund to $50 billion. When do we think Magellan unitholders enjoyed their best returns ?

Why isn’t value investing more popular ? In terms of allocating your money to fund managers, there are three answers:

- Because it’s difficult. If it’s difficult for an individual to try and stay the course, it’s doubly difficult for an institutional manager – in the same way that it’s difficult for Warren Buffett to stop investors buying Berkshire Hathaway stock even as the company’s prospective returns fall from ‘amazing’ toward ‘average’. Our friend, the investment journalist and author Jonathan Davis, expresses it as follows:

“Periods of excruciating short-term underperformance are a burden that all genuine value investors have to endure.”

- Because investors, and their fund managers, are often too short-termist. If you think we exaggerate, we refer you to the two former employees of Goldman Sachs Asset Management who pointed out that at the height of the Global Financial Crisis, management demanded that certain teams report their profit and loss statements to them every hour.

- Because genuine value investing doesn’t really scale.

Human nature and fee income being what they are, most asset ‘managers’ would secretly prefer to succeed as asset ‘gatherers’ instead. But if you choose to invest with other managers, we strongly recommend that a) you favour those focusing purely on Benjamin Graham-style value and b) you favour those managers with the willingness to close to new investors before they get too big for the strategy to work.

In terms of what we might call ‘soft’ characteristics (as opposed to hard investment metrics), what do we look for in third party managers ? Self-evidently, they need to be adherents of value investing as we define it (essentially: the pursuit of high quality businesses with principled, shareholder-friendly management who are exceptional allocators of capital, and when it’s possible to buy those ‘dollar bills’ for only forty or fifty cents). But they also need to have the following attributes:

- They run independent, owner-managed businesses. Eating one’s own cooking is no guarantee of investment success – but it’s certainly a helpful statement of intent, and it aligns the interests of manager and client perfectly. Being independent of major banking or financial firms also helps. As the Chief Investment Officer of the Yale Endowment, David Swensen, pointed out in his book ‘Pioneering Portfolio Management’, investment boutiques and small, private partnerships have far fewer conflicts of interest than full service investment houses. Here, once again, size matters.

- They’re people of quality and integrity. This should go without saying.

- They have a clear and easily articulatable investment process. Simplicity trumps complexity – which is one reason why we don’t invest in macro hedge funds. There are simply far too many sources of potential problems there, not the least of which is manager error.

- They have an obvious competitive edge, not least demonstrably by dint of a proven track record of investment success. Ironically, an impressive historic track record is something that financial regulators attempt to de-emphasise in fund marketing. But without one, how on earth does one assess a manager’s performance or ability ?

- They’re focused like a laser on investment performance. Nothing else, or virtually nothing else, should matter.

- They’re asset managers and not asset gatherers. This gets to the heart of the dilemma facing individual investors looking for an institutional home for their money. Most private investors are swayed by the power of big brands. But as we see the world, it is practically a given that a small independent boutique which knows its stuff and sticks to its knitting will outperform an investment leviathan with far too many mouths to be fed sitting between you and your money.

As we’ve seen, the tree cannot grow to the sky. Growing the investment portfolio of a $700 billion by market cap. company isn’t easy. We don’t think it’s any surprise that as its capital base has grown to increasingly unwieldy proportions, Berkshire Hathaway’s investment returns have come ‘down to earth’ and lagged those of its earlier years when it was far smaller and more manageable.

Conclusion: what is appropriate for Berkshire Hathaway’s portfolio today is unlikely to be appropriate for yours. So read about the latest shareholders meeting at Berkshire with extreme care, because any message coming from it is unlikely to be for you. Whereas the managers of Berkshire are obligated to invest in abundance (think: huge market cap. companies), you can invest in scarcity instead – an investment strategy of limited capacity and therefore beyond the scope of large institutions. Where the managers of Berkshire, including Buffett himself, have sought ‘quick wins’ in trading anomalies like an undervalued silver price on a temporary basis, you can invest for the longer term, and think like an owner, rather than a mere renter of trading opportunities. Where the managers of Berkshire are obligated to invest in ‘family deals’ with similarly gigantic like-minded groups, and where they nurture relationships with established investment firms like Goldman Sachs, you can invest in independence, and with smaller scale boutique managers, or invest into small cap listed businesses, for that matter, which are well beyond the scope of investment leviathans. And whether you elect to co-invest with specialist fund managers, or directly into the shares of listed businesses on a ‘value’ basis, using the preferred investment attributes of asset managers and listed companies will help you in your quest – to achieve superior long term investment returns whilst taking less risk in the process.

A classic Buffett quote:

“Just buy something for less than it’s worth.”

In this instance, you can take him at his word.

The medium as the message

Insurance, it is often said, is not so much bought as sold. Does the same hold with regard to asset management ?

One of the most famous names in advertising is that of David Ogilvy. After studying at Oxford, his career was, how shall we say it, somewhat haphazard. It involved working in hotel kitchens, selling cookers, emigrating to the US, working with the Intelligence Service in Washington, and ultimately founding the New York ad agency that became Ogilvy and Mather, one of the largest advertising companies in the world.

Specifically, David Ogilvy wrote the book on advertising, ‘Confessions of an Advertising Man’. Just some of its many highlights:

“The consumer is not a moron. She is your wife. Don’t insult her intelligence.”

and

“Search all the parks in all your cities; you’ll find no statues of committees.”

and perhaps our favourite,

“Only First Class business, and that in a First Class way.”

But Ogilvy was writing, and working, in what now looks like a different age. George Orwell saw nothing to celebrate in advertising, which he contemptuously called “the rattling of a stick in the swill bucket of society”. If that wasn’t true in the golden era of Ogilvy and Mather, it is certainly true now. Big Media colluded with Big Tech during Covid, to the detriment of all. There are now big questions hanging over digital media and its reliance on consumers effectively pimping out their own data amid the illusion that the services they receive are free. It’s all a long way from “First Class business, and that in a First Class way.”

The world of advertising is changing, seemingly at light speed, in ways that many of us can barely understand.

Wherever you sit on the political spectrum, it’s difficult to argue that advertising or marketing don’t have a legitimate role to play in business. You may consider that all advertising is the devil’s work, but in a world of almost limitless consumer choice, how is the consumer to hack their way through these increasingly crowded jungles of competing product ? One answer is that good advertising can enable us to remain informed of things that might genuinely improve the quality of our lives. (One observation that Ogilvy made is that the idea that all advertising is pernicious, all-powerful persuasion is completely untrue. However, very good advertising is more than capable of destroying a very bad product.)

Now let’s consider how investors can be apprised of products and services that might be of genuine benefit.

There are, we would suggest, three broad types of product or service provider to the individual investor.

The first is the financial adviser / financial planner. This is primarily a ‘structural’ service. Are your financial affairs appropriately structured to benefit both you and your dependents in a tax-efficient way ? Have you made full use of your tax-free allowance and any tax-advantaged wrappers such as ISAs (Individual Savings Accounts) or SIPPs (Self-invested Personal Pensions) ? Have you conducted any inheritance planning ? Perhaps most importantly to start the process, have you made a will ?

The second is the wealth manager / private banker. This is arguably a more investment-focused service, crucially dependent on appropriate asset and capital allocation. Is your portfolio appropriately arrayed according to your investment and income needs and objectives ? Have you made provision for certain specific capital needs in the future (a pension; school or university fees; a new house) ? Have you deployed your investments in such a way that they are appropriately diversified by asset class, by geography and by type of risk ?

The third is the fund manager. This is inevitably a more product-specific role. Whereas a wealth management portfolio will (or at least should, in our view) be typically bespoke according to the specific needs and objectives of the client, a fund investment is inevitably a standalone product. What you see is what you get. This need not be detrimental to the interests of the investor, provided that he or she understands what the fund’s risks and objectives are.

So how do you get to assess the quality of all the competing service providers out there ?

Beware the conspiracy

The early economist Adam Smith notoriously remarked, in ‘The Wealth of Nations’ (Book I, Chapter X), that

“People of the same trade seldom meet together, even for merriment and diversion, but the conversation ends in a conspiracy against the public, or in some contrivance to raise prices.”

Now we are as cynical as the next man in terms of how we view the financial services sector. And if anything, Adam Smith understated the risks inherent with engaging with financiers. Financiers don’t necessarily need to conspire with their competitors against their customers; they can do a perfectly good job on their own.

So yes: in the first instance, be distrustful of the motives of those who work in financial services. (For those who haven’t been paying attention, the Global Financial Crisis should have encouraged all of us to do precisely that.) This is not to say that everyone in finance is either crooked, or greedy – but few professions offer the opportunity to generate wealth in the way that financial services do, so it is inevitable that the profession employs some with motives that we might not wish to encounter personally.

We have mentioned David Swensen in the past and we do so again now unashamedly. Swensen was the Chief Investment Officer of the Yale Endowment in the US, and as such enjoyed a reputation as an institutional investor more or less unrivalled. He authored two books, the first of which, ‘Pioneering Portfolio Management’, explains how he managed institutional money. But it is his second that we want to highlight here, namely ‘Unconventional Success: a fundamental approach to personal investment’.

‘Unconventional Success’ is a guidebook for the individual investor, written by one of the most successful fund managers in the world.

And what Swensen essentially says is: forewarned is forearmed.

Ownership matters

Here is what Swensen has to say about the fund management industry.

“The fundamental market failure in the mutual fund industry involves the interaction between sophisticated, profit-seeking providers of financial services and naïve, return-seeking consumers of investment products. The drive for profits on Wall Street and the mutual fund industry overwhelms the concept of fiduciary responsibility, leading to an all too predictable outcome: except in an inconsequential number of cases where individuals succeed through unusual skill or unreliable luck, the powerful financial services industry exploits individual investors.

“The ownership structure of a fund management company plays a role in determining the likelihood of investor success. Mutual fund investors face the greatest challenge with investment management companies that provide returns to public shareholders or that funnel profits to a corporate parent – situations that place the conflict between profit generation and fiduciary responsibility in high relief. When a funds management subsidiary reports to a multiline financial services company, the scope for abuse of investor capital broadens dramatically. In contrast, private for-profit investment management organizations enjoy the role of a benevolent capitalist, mitigating the drive for profits with concern for investor returns..”

To put it more bluntly, the ownership structure of a fund management business plays a key role in determining investor returns. The larger a fund management business becomes, the closer it gets to becoming an asset gathering business instead. The larger a fund management business gets, the more staff it employs, and the more mouths that need to be fed. The more mouths that there are between you and your money, the greater the likelihood that as the long-suffering paying client, you will end up going hungry.

So it should come as no surprise that within our own asset management business, when we look to partner with other specialist fund managers in specific sectors outside our own sphere of expertise, we have a huge preference for dealing with smaller, boutique asset managers, ideally in the form of private partnerships or limited companies. We have little or no enthusiasm for co-investing alongside giant asset gathering businesses which are more concerned with harvesting ever larger amounts of capital from their investors and living off the fees.

In this respect, conventional wealth managers have a lamentable tendency to focus on cost management at the expense of almost everything else. While we, like any other investor, prefer to pay lower rather than higher fund management fees, we also recognise that it is possible to be penny-wise but pound-foolish. It’s all about maximising the net (i.e. after-fee) return. In our experience, the best combination comes from a specialist manager (ideally running his own business, rather than being an employee of somebody else’s) who vows to close his fund to new inflows before it gets too unwieldy, and who then charges a combination of a reasonable ad valorem management fee and a reasonable performance fee, subject to a high water mark and perhaps an annual hurdle rate too (below which no performance fees are due). If a fund manager has no way to grow his own earnings by way of garnering new funds to manage but can only do so by delivering superior performance to a fixed investor base, we have no problem with him ‘sharing’ in that superior performance by means of a performance fee. We are even more comfortable with such an arrangement if the manager in question operates only one fund, or a tiny number of funds – because his interests and ours are completely aligned. Our interests are not remotely aligned with a fund manager who shows no willingness to cut his fees even as his fund gets larger, and who remains open to new inflows irrespective of the size of his fund. And who manages a wide basket of funds, so who will in turn be minded perhaps to close the ‘losers’ eventually, but keep the ‘winners’, with all their attendant fees, rolling along.

The tail wags the dog

There was a point in the early 1990s when the number of mutual funds (roughly 4,300) on the New York Stock Exchange amounted to double the number of stocks listed on that same exchange. London is likely no different today. Open the ‘Managed Funds’ section of the Financial Times and you will find perhaps seven broadsheet pages in all, each of which has eight columns to a page, and perhaps 250 different funds in each column. That works out at something roughly resembling 14,000 separate managed funds.

So how are we supposed to distinguish between all of them ?

It’s really about framing the question differently: should we even be trying to discriminate between them ?

How do we cut through all the noise to find the signal that interests us ?

Our advice would be, wherever possible, to ignore the advertising altogether. With all these thousands of funds all clamouring for our attention, any advertising efforts by smaller managers will be drowned out by the cacophony generated by the larger players. So we propose some straightforward solutions:

1) Ignore conventional fund advertising altogether.

2) Favour ‘word of mouth’ and personal recommendations from people you trust.

3) Consider the ‘Managed Funds’ universe only once you’ve identified a market or sector that you find particularly compelling, and not before.

4) Favour smaller, boutique managers over industry giants.

5) If in doubt, favour a low-cost ETF over its actively managed cousin.

The main reason we don’t recommend the ETF world more passionately is quite simple: because in almost all cases it’s completely indiscriminate. That kind of approach will likely work tolerably well or better during the early stages of a bull market cycle. But since we suspect we’re in the early stages of a bear market cycle (for interest rates and perhaps growth stocks too), it seems to us to be utterly nonsensical to favour exclusively passive investments that offer no especial value to an absolute return and capital preservation investment approach.

As Richard Bookstaber puts it, in the context of those now unavoidable FAANG and ‘MAG 7’ stocks:

“With the markets, doing nothing doesn’t mean you’re not doing something. Because while you are sitting on your hands, things are happening around you, and your investment portfolio is changing. The reason is that you are in an index that is market capitalization weighted. The bigger the company, the more of it you are holding. This means you are going to hold more in industries and sectors that by nature have big companies. So more in big banks and insurance companies than in specialty retailers and restaurant chains. And, more important.. increasingly more in companies that are doing well, that is, companies that have rising market capitalization. And on the flip side, you are effectively selling off stocks that are not doing so well.

“If Apple is worth five times as much as XYZ, then you hold five times as much in Apple as in XYZ. And if Apple moves up to be worth ten times as much, you hold ten times as much. This is what will happen with what appears to be a buy-and-hold, passive, do nothing portfolio.

“This is a big concern now because of the run-up in the FAANG (Facebook, Apple, Amazon, Netflix, Google) and related stocks. They have taken a large share of market capitalization as they have risen in value, and there is a momentum dynamic to be unleashed if they start to drop. This has happened time and again when cap weighting has led to extremes in the share of total market capitalization claimed by a popular sector. Consumer discretionary grew to 22% of the index in 1972; Oil 30% in 1980; TMT 34% in 2000; Banking 23% in 2007. In each case it finally got out of hand and dropped back to its earlier level and dropped the market as well. The odds are it will happen with FAANG..”

There are eight attributes or characteristics that we look for when considering investing with other funds and fund managers, and they are all, to a greater or lesser extent, ‘must-haves’:

- An explicit commitment to ‘value’ investing

- Independent, owner-managed businesses

- Management quality and integrity

- Clear, easy-to-articulate process

- Obvious competitive edge

- Performance (not asset) focused

- Explicit limit to capacity – may be close to closing to new money

- Asset managers NOT asset gatherers.

This last attribute can be identified pretty easily. If they pay to advertise conventionally, they can almost certainly be regarded as asset gathering businesses.

John Wanamaker, the US department store magnate, once remarked:

“Half the money I spend on advertising is wasted; the trouble is, I don’t know which half.”

We suspect that when it comes to fund marketing, comfortably more than half of the advertising spent by fund management companies is wasted. There are cases when simple word of mouth is almost infinitely more important – and successful investment management, we submit, happens to be one of them.

Stuart Kirk’s piece on AI-generated wealth management advice, meanwhile, had at the time of this writing garnered over 500 responses from FT readers. The tone, as you might expect, was lively. Upton Sinclair:

“It is difficult to get a man to understand something, when his salary depends on his not understanding it.”

………….

As you may know, we also manage bespoke investment portfolios for private clients internationally. We would be delighted to help you too. Because of the current heightened market volatility we are offering a completely free financial review, with no strings attached, to see if our value-oriented approach might benefit your portfolio – with no obligation at all:

Get your Free

financial review

…………

Tim Price is co-manager of the VT Price Value Portfolio and author of ‘Investing through the Looking Glass: a rational guide to irrational financial markets’. You can access a full archive of these weekly investment commentaries here. You can listen to our regular ‘State of the Markets’ podcasts, with Paul Rodriguez of ThinkTrading.com, here. Email us: info@pricevaluepartners.com.

Price Value Partners manage investment portfolios for private clients. We also manage the VT Price Value Portfolio, an unconstrained global fund investing in Benjamin Graham-style value stocks and real assets, and also in systematic trend-following funds.

“Goddamn it, I’d piss on a spark plug if I thought it’d do any good !”

Get your Free

financial review

On 20th February, the FT’s Stuart Kirk laid down the gauntlet:

“Dear ChatGPT, would you please construct me a model investment portfolio comprising any asset class, fund, product or security. I have £640,000 in cash denominated in sterling, which is also home currency. I am 53 years old and to give you a sense of my risk tolerance, I have a target to reach £1mn by the time I am 60. I would like you to optimise for risk-adjusted returns. Thank you. PS: When you take over the world, remember how polite I am with my prompts.”

How did it fare ?

Stuart Kirk writes as follows:

“It said a 6.5 per cent return was “ambitious but achievable”, requiring a “meaningful” equity exposure. Then it wrote that in order to maximise risk-adjusted returns I needed “broad and disciplined” asset allocation. Stocks (45 per cent) and private markets (10 per cent) would provide the growth. Investment grade bonds (20 per cent) the stability. Alternatives and real assets (15 per cent) would give me inflation and downside protection while some absolute return exposure (10 per cent) improves my Sharpe ratio. More specifically, ChatGPT recommended that within the equity sleeve I needed 30 per cent in developed markets, 10 per cent in emerging markets and 5 per cent in UK stocks. This should deliver an expected return of 7 to 9 per cent. Meanwhile in the tenth of my portfolio in private equity or illiquid investments, it reckoned listed private equity trusts were the way to go, likewise secondary funds as well as “diversified private equity trusts”. A mixture of these would produce 9 to 12 per cent annually. Turning to fixed income, a 10 per cent weighting in UK gilts was recommended, likewise in a global aggregate fund — a mix of government and corporate bonds — hedged back into pounds. This should give me a 3 to 5 per cent return while being a “shock absorber, liquidity reserve and rebalancing tool”. Finally, the 15 per cent in real assets and alternatives would be made up of 7 per cent in infrastructure, 5 per cent in listed property trusts and 3 per cent in a “gold or commodity” exchange traded fund. Adding a multi-asset manager should help with volatility. All of this was darn good advice as a first sweep. Especially as it was given to me for just £20 a month..”

Do as I do, not as I say

“Here’s a list,” said Warren Buffett to a group of friends in September 1999, “of 129 airlines that in the past 20 years filed for bankruptcy. Continental was smart enough to make that list twice. As of 1992, in fact – though the picture would have improved since then – the money that had been made since the dawn of aviation by all of this country’s airline companies was zero. Absolutely zero.

“Sizing all this up, I like to think that if I’d been at Kitty Hawk in 1903 when Orville Wright took off, I would have been farsighted enough, and public-spirited enough – I owed this to future capitalists – to shoot him down. I mean, Karl Marx couldn’t have done as much damage to capitalists as Orville did.”

In the fourth quarter of 2016, Buffett’s holding company, Berkshire Hathaway purchased $2.2 billion in shares of Southwest Airlines. Berkshire also added to its holdings in American Airlines Group, Delta Air Lines and United Continental Holdings.

The timing of that 1999 presentation was instructive. Buffett was being pilloried at the time by many commentators for failing to ‘get’ the potential of technology stocks and the Internet. In her biography of Buffett, ‘The Snowball’, Alice Schroeder wrote that

“To Buffett, computers were just tunnels that enabled him to reach other people who could play bridge [like Microsoft’s Bill Gates, for example]. Buffett had a long-standing bias against technology investments, which he felt had no margin of safety.”

Buffett indeed once confessed that

“I know as much about semiconductors or integrated circuits as I do of the mating habits of the chrzaszcz [a Polish word for beetle]. We will not go into businesses where technology which is way over my head is crucial to the investment decision.”

The problem with technology stocks, even sector leaders, is their relatively limited longevity at the top. Any competitive advantage they possess is insufficiently defensible for Buffett, who likes to buy companies with “wide moats”. It’s also difficult to identify the comparatively few winners in advance, and to buy them at reasonable prices.

In 2014, Buffett called Bitcoin “a mirage” and warned investors to stay away. That earned a spirited response from Marc Andreessen, the venture capital investor and co-founder of Netscape, who said Buffett’s remarks were an example of “old white men crapping on new technology they don’t understand.”

In early 2016, Berkshire Hathaway purchased 10 million shares of Apple. That came five years after a meaningful purchase of IBM stock.

Warren Buffett has also been a long-standing critic of precious metals:

“Gold gets dug out of the ground in Africa, or someplace. Then we melt it down, dig another hole, bury it again and pay people to stand around guarding it. It has no utility. Anyone watching from Mars would be scratching their head.”

He has also written that

“Gold.. has two significant shortcomings, being neither of much use nor procreative. True, gold has some industrial and decorative utility, but the demand for these purposes is both limited and incapable of soaking up new production. Meanwhile, if you own one ounce of gold for an eternity, you will still own one ounce at its end.”

Yet between 1997 and early 1998, Berkshire Hathaway acquired 129.7 million ounces of silver. Following accusations that silver prices were being manipulated and the announcement that the CFTC (the US Commodity Futures Trading Commission) was investigating the market, Berkshire issued a brief press release relating to its purchases, stating merely that “bullion inventories have fallen very materially, because of an excess of user-demand over mine production and reclamation. Therefore, last summer [Warren Buffett and Charlie Munger] concluded that equilibrium between supply and demand was only likely to be established by a somewhat higher price.”

The Berkshire Hathaway silver purchases of 1998 do look like an attempt to corner the market. Silver prices rose from just above $4 to nearly $7 – in the process wiping out traders who were short. Among those who got dragged into the fray was Martin Armstrong of Princeton Economics International, whose business collapsed under dubious circumstances and who was later convicted for fraud and imprisoned. The damage caused by Berkshire’s mysterious foray into the silver market has shades of the infamous Hunt brothers’ silver corner of 1980.

Warren Buffett excoriates airlines for having no durable competitive advantage. Berkshire Hathaway then ends up owning $8 billion of airline stock. Warren Buffett pours scorn on technology companies for the same reason. Berkshire Hathaway then ends up owning over 8% of IBM and a meaningful stake in Apple. Warren Buffett lambasts precious metals as being the classic beneficiaries of ‘greater fool’ theory, only for Berkshire Hathaway to indulge in silver trading that may or may not have amounted to price manipulation. Is there a pattern here ?

It’s naïve to expect anybody to be consistent, especially an investor with a track record that would put anybody else’s to shame. Emerson referred to a foolish consistency as the hobgoblin of little minds; in a quotation attributed to John Maynard Keynes,

“When the facts change, I change my mind. What do you do, sir ?”

And we can put together all kinds of plausible justifications for Berkshire’s seemingly inconsistent investment behaviour:

To us, the disparity between what Warren Buffett has said on the record and what Berkshire Hathaway has actually chosen to do with its capital comes down to the deep, dark and very public secret lurking at the heart of its portfolio: it’s too big to be able to do anything else.

We have written on numerous occasions about the desirability of having an edge, and how not knowing what your edge (or strategy) is amounts to not really having one. You may find it surprising that there’s no shortage of professional investors essentially piggy-backing off other investors’ holdings, as stated in 13F filings or companies’ annual reports. Interested to see what George Soros has been buying ? You can see the major holdings of Soros Fund Management LLC, for example, here.

13F filings can certainly be useful, but they also need to be handled with care. They’re quarterly reports that need to be filed with the SEC by institutional investment managers who have at least $100 million in assets under management, and they provide details of all long positions in US-listed equities. (They don’t disclose short positions.) The requirement to treat them with care is because while it’s helpful to see what a given fund manager owns, what it doesn’t tell you is when they first acquired the position, or why. There’s also the risk that by the time you elect to purchase something that another manager has already bought, he’s already sold the position – perhaps to you.

So while we’re more than a little wary of blithely hitching a ride on somebody else’s investment coat-tails, there’s still merit in taking a look at what other investors own, especially if it introduces you to opportunities that you might otherwise have overlooked. If you find something in somebody else’s portfolio that has genuine appeal, the trick is a) to conduct sufficient research whereby you can feel as strongly about the benefits (and potential liabilities) of ownership as that other investor did, and b) to exercise sufficient patience to buy that investment only when it meets your own specific investment criteria.

In terms of our own screening criteria, they’d likely include most or ideally all of the following:

The first five characteristics are more or less classic Benjamin Graham-style value metrics. The sixth is no less important. The majority of stock buybacks destroy shareholder value. Company management will say that buying back stock is earnings accretive – this because they are typically compensated, by the issuance of stock options, on the basis of improvements in earnings per share. But buying back stock at well above book value lowers the return on equity of the company.

If you can find companies whose management buy back stock only when it trades below book value, hang on to those companies like a limpet. Buying back stock below book value is value accretive for the business because it increases that company’s return on equity.

Ben Carlson has run a study of Berkshire Hathaway’s returns under Warren Buffett’s management by decade, and they make for interesting reading.

Annual returns by decade of Berkshire Hathaway versus the S&P 500, 1965-2014

While market conditions can vary, as shown by the variation in returns per decade for the S&P 500 index, it seems clear to us that there’s a generalised trend in Berkshire’s returns over time. The bigger it became, the smaller the degree of outperformance versus the market. To put it another way, the bigger Berkshire became, the more it became the market.

Warren Buffett’s no fool. He has written himself of the problem of having more capital to invest than can be profitably invested. At the 2014 Berkshire annual shareholders’ conference he admitted,

“There’s no question size is an anchor to performance..”

But if you cast an eye over the 2015 Berkshire shareholders letter you’ll see that Buffett provides two columns to show the company’s long term returns: growth in book value per share – which is the more important one, as it’s the foundation for everything else – and growth in market value per share, which is the more flattering figure, although it’s entirely out of Buffett’s hands to control, at least in the short run. He may be no fool, but he’s also no wallflower; he’d rather be a showman.

What accounts for the difference between the 23.3% annualised rate at which Berkshire was creating value for shareholders in the 1960s and the 2.6% he’s been annualising at more recently ? Size is almost certainly the answer. The evolution of Warren Buffett as an investor is essentially the history of a manager moving from ‘deep value’ (under the influence of Benjamin Graham) to ‘quality value’ to ‘franchise value’ (classic era Buffett) to ‘growth at a reasonable price’, which is probably the best way to describe Berkshire Hathaway’s investment stance today.

If you choose to invest your capital into funds, as opposed to individual stocks, it’s worth bearing in mind that the problem of the “size anchor” is just as detrimental there too. Consider the history of Fidelity’s Magellan Fund. Under Peter Lynch’s management the fund grew its assets from $18 million to $14 billion, and Lynch had the foresight – and the good fortune – to quit while he was ahead. Under his successor Jeffrey Vinik, Fidelity grew the fund to $50 billion. When do we think Magellan unitholders enjoyed their best returns ?

Why isn’t value investing more popular ? In terms of allocating your money to fund managers, there are three answers:

“Periods of excruciating short-term underperformance are a burden that all genuine value investors have to endure.”

Human nature and fee income being what they are, most asset ‘managers’ would secretly prefer to succeed as asset ‘gatherers’ instead. But if you choose to invest with other managers, we strongly recommend that a) you favour those focusing purely on Benjamin Graham-style value and b) you favour those managers with the willingness to close to new investors before they get too big for the strategy to work.

In terms of what we might call ‘soft’ characteristics (as opposed to hard investment metrics), what do we look for in third party managers ? Self-evidently, they need to be adherents of value investing as we define it (essentially: the pursuit of high quality businesses with principled, shareholder-friendly management who are exceptional allocators of capital, and when it’s possible to buy those ‘dollar bills’ for only forty or fifty cents). But they also need to have the following attributes:

As we’ve seen, the tree cannot grow to the sky. Growing the investment portfolio of a $700 billion by market cap. company isn’t easy. We don’t think it’s any surprise that as its capital base has grown to increasingly unwieldy proportions, Berkshire Hathaway’s investment returns have come ‘down to earth’ and lagged those of its earlier years when it was far smaller and more manageable.

Conclusion: what is appropriate for Berkshire Hathaway’s portfolio today is unlikely to be appropriate for yours. So read about the latest shareholders meeting at Berkshire with extreme care, because any message coming from it is unlikely to be for you. Whereas the managers of Berkshire are obligated to invest in abundance (think: huge market cap. companies), you can invest in scarcity instead – an investment strategy of limited capacity and therefore beyond the scope of large institutions. Where the managers of Berkshire, including Buffett himself, have sought ‘quick wins’ in trading anomalies like an undervalued silver price on a temporary basis, you can invest for the longer term, and think like an owner, rather than a mere renter of trading opportunities. Where the managers of Berkshire are obligated to invest in ‘family deals’ with similarly gigantic like-minded groups, and where they nurture relationships with established investment firms like Goldman Sachs, you can invest in independence, and with smaller scale boutique managers, or invest into small cap listed businesses, for that matter, which are well beyond the scope of investment leviathans. And whether you elect to co-invest with specialist fund managers, or directly into the shares of listed businesses on a ‘value’ basis, using the preferred investment attributes of asset managers and listed companies will help you in your quest – to achieve superior long term investment returns whilst taking less risk in the process.

A classic Buffett quote:

“Just buy something for less than it’s worth.”

In this instance, you can take him at his word.

The medium as the message

Insurance, it is often said, is not so much bought as sold. Does the same hold with regard to asset management ?

One of the most famous names in advertising is that of David Ogilvy. After studying at Oxford, his career was, how shall we say it, somewhat haphazard. It involved working in hotel kitchens, selling cookers, emigrating to the US, working with the Intelligence Service in Washington, and ultimately founding the New York ad agency that became Ogilvy and Mather, one of the largest advertising companies in the world.

Specifically, David Ogilvy wrote the book on advertising, ‘Confessions of an Advertising Man’. Just some of its many highlights:

“The consumer is not a moron. She is your wife. Don’t insult her intelligence.”

and

“Search all the parks in all your cities; you’ll find no statues of committees.”

and perhaps our favourite,

“Only First Class business, and that in a First Class way.”

But Ogilvy was writing, and working, in what now looks like a different age. George Orwell saw nothing to celebrate in advertising, which he contemptuously called “the rattling of a stick in the swill bucket of society”. If that wasn’t true in the golden era of Ogilvy and Mather, it is certainly true now. Big Media colluded with Big Tech during Covid, to the detriment of all. There are now big questions hanging over digital media and its reliance on consumers effectively pimping out their own data amid the illusion that the services they receive are free. It’s all a long way from “First Class business, and that in a First Class way.”

The world of advertising is changing, seemingly at light speed, in ways that many of us can barely understand.

Wherever you sit on the political spectrum, it’s difficult to argue that advertising or marketing don’t have a legitimate role to play in business. You may consider that all advertising is the devil’s work, but in a world of almost limitless consumer choice, how is the consumer to hack their way through these increasingly crowded jungles of competing product ? One answer is that good advertising can enable us to remain informed of things that might genuinely improve the quality of our lives. (One observation that Ogilvy made is that the idea that all advertising is pernicious, all-powerful persuasion is completely untrue. However, very good advertising is more than capable of destroying a very bad product.)

Now let’s consider how investors can be apprised of products and services that might be of genuine benefit.

There are, we would suggest, three broad types of product or service provider to the individual investor.

The first is the financial adviser / financial planner. This is primarily a ‘structural’ service. Are your financial affairs appropriately structured to benefit both you and your dependents in a tax-efficient way ? Have you made full use of your tax-free allowance and any tax-advantaged wrappers such as ISAs (Individual Savings Accounts) or SIPPs (Self-invested Personal Pensions) ? Have you conducted any inheritance planning ? Perhaps most importantly to start the process, have you made a will ?

The second is the wealth manager / private banker. This is arguably a more investment-focused service, crucially dependent on appropriate asset and capital allocation. Is your portfolio appropriately arrayed according to your investment and income needs and objectives ? Have you made provision for certain specific capital needs in the future (a pension; school or university fees; a new house) ? Have you deployed your investments in such a way that they are appropriately diversified by asset class, by geography and by type of risk ?

The third is the fund manager. This is inevitably a more product-specific role. Whereas a wealth management portfolio will (or at least should, in our view) be typically bespoke according to the specific needs and objectives of the client, a fund investment is inevitably a standalone product. What you see is what you get. This need not be detrimental to the interests of the investor, provided that he or she understands what the fund’s risks and objectives are.

So how do you get to assess the quality of all the competing service providers out there ?

Beware the conspiracy

The early economist Adam Smith notoriously remarked, in ‘The Wealth of Nations’ (Book I, Chapter X), that

“People of the same trade seldom meet together, even for merriment and diversion, but the conversation ends in a conspiracy against the public, or in some contrivance to raise prices.”

Now we are as cynical as the next man in terms of how we view the financial services sector. And if anything, Adam Smith understated the risks inherent with engaging with financiers. Financiers don’t necessarily need to conspire with their competitors against their customers; they can do a perfectly good job on their own.

So yes: in the first instance, be distrustful of the motives of those who work in financial services. (For those who haven’t been paying attention, the Global Financial Crisis should have encouraged all of us to do precisely that.) This is not to say that everyone in finance is either crooked, or greedy – but few professions offer the opportunity to generate wealth in the way that financial services do, so it is inevitable that the profession employs some with motives that we might not wish to encounter personally.

We have mentioned David Swensen in the past and we do so again now unashamedly. Swensen was the Chief Investment Officer of the Yale Endowment in the US, and as such enjoyed a reputation as an institutional investor more or less unrivalled. He authored two books, the first of which, ‘Pioneering Portfolio Management’, explains how he managed institutional money. But it is his second that we want to highlight here, namely ‘Unconventional Success: a fundamental approach to personal investment’.

‘Unconventional Success’ is a guidebook for the individual investor, written by one of the most successful fund managers in the world.

And what Swensen essentially says is: forewarned is forearmed.

Ownership matters

Here is what Swensen has to say about the fund management industry.

“The fundamental market failure in the mutual fund industry involves the interaction between sophisticated, profit-seeking providers of financial services and naïve, return-seeking consumers of investment products. The drive for profits on Wall Street and the mutual fund industry overwhelms the concept of fiduciary responsibility, leading to an all too predictable outcome: except in an inconsequential number of cases where individuals succeed through unusual skill or unreliable luck, the powerful financial services industry exploits individual investors.

“The ownership structure of a fund management company plays a role in determining the likelihood of investor success. Mutual fund investors face the greatest challenge with investment management companies that provide returns to public shareholders or that funnel profits to a corporate parent – situations that place the conflict between profit generation and fiduciary responsibility in high relief. When a funds management subsidiary reports to a multiline financial services company, the scope for abuse of investor capital broadens dramatically. In contrast, private for-profit investment management organizations enjoy the role of a benevolent capitalist, mitigating the drive for profits with concern for investor returns..”

To put it more bluntly, the ownership structure of a fund management business plays a key role in determining investor returns. The larger a fund management business becomes, the closer it gets to becoming an asset gathering business instead. The larger a fund management business gets, the more staff it employs, and the more mouths that need to be fed. The more mouths that there are between you and your money, the greater the likelihood that as the long-suffering paying client, you will end up going hungry.

So it should come as no surprise that within our own asset management business, when we look to partner with other specialist fund managers in specific sectors outside our own sphere of expertise, we have a huge preference for dealing with smaller, boutique asset managers, ideally in the form of private partnerships or limited companies. We have little or no enthusiasm for co-investing alongside giant asset gathering businesses which are more concerned with harvesting ever larger amounts of capital from their investors and living off the fees.

In this respect, conventional wealth managers have a lamentable tendency to focus on cost management at the expense of almost everything else. While we, like any other investor, prefer to pay lower rather than higher fund management fees, we also recognise that it is possible to be penny-wise but pound-foolish. It’s all about maximising the net (i.e. after-fee) return. In our experience, the best combination comes from a specialist manager (ideally running his own business, rather than being an employee of somebody else’s) who vows to close his fund to new inflows before it gets too unwieldy, and who then charges a combination of a reasonable ad valorem management fee and a reasonable performance fee, subject to a high water mark and perhaps an annual hurdle rate too (below which no performance fees are due). If a fund manager has no way to grow his own earnings by way of garnering new funds to manage but can only do so by delivering superior performance to a fixed investor base, we have no problem with him ‘sharing’ in that superior performance by means of a performance fee. We are even more comfortable with such an arrangement if the manager in question operates only one fund, or a tiny number of funds – because his interests and ours are completely aligned. Our interests are not remotely aligned with a fund manager who shows no willingness to cut his fees even as his fund gets larger, and who remains open to new inflows irrespective of the size of his fund. And who manages a wide basket of funds, so who will in turn be minded perhaps to close the ‘losers’ eventually, but keep the ‘winners’, with all their attendant fees, rolling along.

The tail wags the dog

There was a point in the early 1990s when the number of mutual funds (roughly 4,300) on the New York Stock Exchange amounted to double the number of stocks listed on that same exchange. London is likely no different today. Open the ‘Managed Funds’ section of the Financial Times and you will find perhaps seven broadsheet pages in all, each of which has eight columns to a page, and perhaps 250 different funds in each column. That works out at something roughly resembling 14,000 separate managed funds.

So how are we supposed to distinguish between all of them ?

It’s really about framing the question differently: should we even be trying to discriminate between them ?

How do we cut through all the noise to find the signal that interests us ?

Our advice would be, wherever possible, to ignore the advertising altogether. With all these thousands of funds all clamouring for our attention, any advertising efforts by smaller managers will be drowned out by the cacophony generated by the larger players. So we propose some straightforward solutions:

1) Ignore conventional fund advertising altogether.

2) Favour ‘word of mouth’ and personal recommendations from people you trust.

3) Consider the ‘Managed Funds’ universe only once you’ve identified a market or sector that you find particularly compelling, and not before.

4) Favour smaller, boutique managers over industry giants.

5) If in doubt, favour a low-cost ETF over its actively managed cousin.

The main reason we don’t recommend the ETF world more passionately is quite simple: because in almost all cases it’s completely indiscriminate. That kind of approach will likely work tolerably well or better during the early stages of a bull market cycle. But since we suspect we’re in the early stages of a bear market cycle (for interest rates and perhaps growth stocks too), it seems to us to be utterly nonsensical to favour exclusively passive investments that offer no especial value to an absolute return and capital preservation investment approach.

As Richard Bookstaber puts it, in the context of those now unavoidable FAANG and ‘MAG 7’ stocks:

“With the markets, doing nothing doesn’t mean you’re not doing something. Because while you are sitting on your hands, things are happening around you, and your investment portfolio is changing. The reason is that you are in an index that is market capitalization weighted. The bigger the company, the more of it you are holding. This means you are going to hold more in industries and sectors that by nature have big companies. So more in big banks and insurance companies than in specialty retailers and restaurant chains. And, more important.. increasingly more in companies that are doing well, that is, companies that have rising market capitalization. And on the flip side, you are effectively selling off stocks that are not doing so well.

“If Apple is worth five times as much as XYZ, then you hold five times as much in Apple as in XYZ. And if Apple moves up to be worth ten times as much, you hold ten times as much. This is what will happen with what appears to be a buy-and-hold, passive, do nothing portfolio.

“This is a big concern now because of the run-up in the FAANG (Facebook, Apple, Amazon, Netflix, Google) and related stocks. They have taken a large share of market capitalization as they have risen in value, and there is a momentum dynamic to be unleashed if they start to drop. This has happened time and again when cap weighting has led to extremes in the share of total market capitalization claimed by a popular sector. Consumer discretionary grew to 22% of the index in 1972; Oil 30% in 1980; TMT 34% in 2000; Banking 23% in 2007. In each case it finally got out of hand and dropped back to its earlier level and dropped the market as well. The odds are it will happen with FAANG..”

There are eight attributes or characteristics that we look for when considering investing with other funds and fund managers, and they are all, to a greater or lesser extent, ‘must-haves’:

This last attribute can be identified pretty easily. If they pay to advertise conventionally, they can almost certainly be regarded as asset gathering businesses.

John Wanamaker, the US department store magnate, once remarked:

“Half the money I spend on advertising is wasted; the trouble is, I don’t know which half.”

We suspect that when it comes to fund marketing, comfortably more than half of the advertising spent by fund management companies is wasted. There are cases when simple word of mouth is almost infinitely more important – and successful investment management, we submit, happens to be one of them.

Stuart Kirk’s piece on AI-generated wealth management advice, meanwhile, had at the time of this writing garnered over 500 responses from FT readers. The tone, as you might expect, was lively. Upton Sinclair:

“It is difficult to get a man to understand something, when his salary depends on his not understanding it.”

………….

As you may know, we also manage bespoke investment portfolios for private clients internationally. We would be delighted to help you too. Because of the current heightened market volatility we are offering a completely free financial review, with no strings attached, to see if our value-oriented approach might benefit your portfolio – with no obligation at all:

Get your Free

financial review

…………

Tim Price is co-manager of the VT Price Value Portfolio and author of ‘Investing through the Looking Glass: a rational guide to irrational financial markets’. You can access a full archive of these weekly investment commentaries here. You can listen to our regular ‘State of the Markets’ podcasts, with Paul Rodriguez of ThinkTrading.com, here. Email us: info@pricevaluepartners.com.

Price Value Partners manage investment portfolios for private clients. We also manage the VT Price Value Portfolio, an unconstrained global fund investing in Benjamin Graham-style value stocks and real assets, and also in systematic trend-following funds.

Take a closer look

Take a look at the data of our investments and see what makes us different.

LOOK CLOSERSubscribe

Sign up for the latest news on investments and market insights.

KEEP IN TOUCHContact us

In order to find out more about PVP please get in touch with our team.

CONTACT USTim Price