“The game of speculation is the most uniformly fascinating game in the world. But it is not a game for the stupid, the mentally lazy, the man of inferior emotional balance, or for the get-rich-quick adventurer. They will die poor.”

Get your Free

financial review

There is scandal, self-inflicted economic destruction, cultural malaise and political tension aplenty here at home, and no shortage of it abroad.

With a 40-year bull market in interest rates now in the rear-view mirror, and government debt piles now unmanageably vast, we regard the bond markets as essentially uninvestible. Many stock markets are trading at record levels. AI is a bigger bubble than dotcom 1.0. Did someone use the word risky? As Sergeant Esterhaus would routinely say at the beginning of every episode of the TV police drama Hill Street Blues,

“Let’s be careful out there.”

If you were looking for a form of investment that could offer you protection against a multitude of potentially bad outcomes, what would it look like? What attributes would it have? Here are some of the characteristics we would like to see in such an investment:

- This form of investment would have to be either entirely uncorrelated or slightly negatively correlated to both the stock and bond markets. That is, whatever its future return profile, its price would move completely independently to those of traditional assets.

- This form of investment would have to have an excellent track record of generating meaningful gains over the longer term.

- This form of investment would have to use some of the most sophisticated risk management tools, such that the probability of incurring a meaningful and sustained loss was relatively small.

- This form of investment would have to offer the potential to make meaningful positive returns even and especially in severe bear markets.

If such an investment sounds too good to be true, we have news for you.

There is an investment strategy that has been one of the most consistently profitable in the world – for centuries. It is also one of the most secretive. It is mostly used by a small number of traders who happen to know the strategy – but it doesn’t even require huge amounts of capital. And anyone can be taught the basics in minutes.

First, a relevant cultural aside. The movie ‘Trading Places’ was based on a true story.

If you haven’t seen the film yet, you should. It is one of the funniest comedies about Wall Street ever made – not a huge field, admittedly. In it, two unscrupulous commodity brokers wager that they can take a vagrant (Eddie Murphy) off the street and turn him into a successful trader.

The film was a smash hit, symbolic of a more innocent age (specifically 1983) when interference in innocent people’s lives by gambling financiers was the exception rather than the rule.

At precisely the same time, the commodities trader Richard Dennis set out to show that anybody could become a successful trader provided they were simply taught properly.

His partner, Bill Eckhardt, disagreed – and a wager was born.

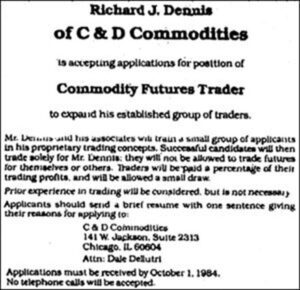

Dennis placed classified ads in the back of Barron’s magazine. This is what they looked like:

Prior experience was not necessary. But applicants did have to complete a psychological profile. Among the test were some true-false questions, such as:

- The majority of traders are always wrong

- It’s good to follow hunches in trading

- It’s good to average down when buying

- A trader should be willing to let profits turn into losses

- Needing and wanting money are good motivators to good trading..

He ended up with two classes of what he called ‘turtles’, named after a visit to a Singaporean turtle farm. Dennis believed that successful traders could be raised, like baby turtles in a vat of water, simply by being taught the fundamental principles of trading.

And Dennis didn’t rig the experiment. Among those selected for the trial were graduates in piano and music theory, an accountant, a geologist, an unemployed guy, and someone from the United States Air Force Academy. Typical business students they were not.

Long story short, Richard Dennis won his bet.

He hired fewer than two dozen novice traders. Jerry Parker was among them. He is now believed to be worth upwards of $700 million.

$1000 invested with fellow ‘turtle’ Tom Shanks’ Hawksbill Capital in 1988 would now be worth something north of $100,000.

Turtles Paul Rabar, Mike Carr, Howard Seidler and Jim DiMaria all set up fantastically successful trading firms after their experience with Dennis.

So what did Dennis teach them ?

There are only two ways consistently to make money from the financial markets. One of them is value investing. Buying high quality assets for less than they’re fundamentally worth is a credible and immensely successful strategy over the medium term.

The other is what we can call momentum.

Old hands in the City and on Wall Street tend to favour fundamental analysis of the markets. They waste their time discussing and debating the future course of the economy, of interest rates, and inflation. This is all very interesting – perhaps – but fundamentals tell you nothing about how to make money. All of that information is already in the price. And fundamentals are also somewhat subjective – take two economists, ask for their opinion, and you’ll get at least three answers.

Another way to look at financial markets is by using technical analysis. This is not as complicated as it might sound. It simply means looking at the price history of financial assets.

The reality, which is something that Dennis intuitively knew, and that he went on to teach his turtles, is that price is the only metric worth trusting. You can have a view about the future path of interest rates, for example. You may think they’re going lower. But that view might be 100% wrong.

Everything else is subjective.

So this is the system that Dennis taught. It’s a trading strategy that today goes by the title of ‘systematic trend-following’.

‘Systematic’ because there’s a clearly articulated system. This is a rules-based approach to trading. For example, one rule might be:

- When a given market trades at a new 52-week high, then buy it.

Another rule might be:

- When a given market trades at a new 52-week low, then sell it.

These are clearly simple examples. A decent ‘systematic, trend-following’ system will likely incorporate a wide variety of rules, incorporating guidance on when to get in, when to get out, and how to size positions.

The point being, once you have established that set of rules, you don’t deviate from them. At all. They can clearly be refined, over time. But they should never, under any account, be abandoned.

Unlike many trading approaches, systematic trend-following requires no special understanding of any given market. In fact, we have a friend with a small trend-following fund who assures us that he’s perfectly happy to trade markets ‘blind’ – he doesn’t even need to know exactly what he’s trading, he just needs to see the price history and he can make his trade entry and exit decisions based on that alone.

Trend-followers are not remotely interested in macro-economic analysis. If they use Wall Street research at all, it will be to prop up a wobbly chair leg.

What does interest trend-followers is catching a ride on big market trends. This is the key to the success of trend-following as an investment (more accurately, trading) strategy. Markets have a tendency to make big moves that come as a complete surprise to most investors. But not to trend-followers: big “surprise” moves is precisely what they live for. It’s the source of their outsized profits. Check out, for example, the cocoa price during 2024 for more on this theme.

Today’s trend-followers are following a path laid down by one of the most successful stock traders in history – Jesse Livermore (1877-1940). Livermore’s nicknames included ‘the Boy Plunger’ and ‘the Great Bear of Wall Street’. Livermore managed to make, and then lose, several fortunes. But he was not a creature of some long-lived bull market, like so many of today’s accidentally successful hedge fund managers. After the 1929 Crash, he ended up worth $100 million, when many of his trading rivals lost everything.

Happily for the wannabe trader today, Jesse Livermore’s approach is just as valid as it’s always been. As he said himself,

“There is nothing new in Wall Street. There can’t be, because speculation is as old as the hills. Whatever happens in the stock market today has happened before and will happen again.”

The US firm Research Affiliates published an excellent piece a while ago entitled “How Not to Get Fired with Smart Beta Investing”. You can read it here.

The piece comes to a number of fascinating conclusions about the history of stock market investing over the past 50 years.

For example, it strongly suggests that “quality” and “growth” style investing (essentially, paying up for global mega-brands, for example, or paying over the odds to buy the shares of fast-growing companies) tends to give you worse returns, over time, than simply buying the market.

And it also suggests that there are two strategies that, over time, offer a high likelihood of beating the market. One of them is “value” (which will hardly be news to longstanding readers). The other is “momentum” – which we can define here simply as “buying what’s going up in price – and, for that matter, selling what’s going down”. Clearly they are almost diametrically opposed as philosophies.

“Value” investing is both qualitative and quantitative, and lays great store in patient, defensive, contrarian investing. “Momentum”, on the other hand, is far closer to a shorter term “trading” approach, driven entirely by price; it barely considers the underlying quality of a business at all. Price momentum is really all it’s worried about – what direction the share price is going, and how strong the trend of that share price movement.

So a combination of “value” and “momentum” approaches probably isn’t a bad idea within a balanced portfolio.

How does a systematic trend-following fund actually work? What precisely does it do?

Perhaps 99% of actively managed funds have managers who attempt to predict the future. They try and assess prospects for the wider economy and forecast the direction of interest rates, currencies and inflation (in the hedge fund world this strategy is known as “global macro”). When it comes to the stock market, most fund managers attempt to predict the growth of specific industry sectors or the profits and prospects of individual companies.

Systematic trend-following managers don’t do any of this.

Instead, they simply track the prices of multiple types of assets – interest rates, currencies, stock indices, hard commodities like iron or zinc, soft commodities like corn or soya beans – and when they (or just as likely their computer algorithm) identify a market in something that’s trending strongly (whether up in price or down they don’t really care), they simply initiate a position in that market, and for as long as the trend continues, they will add to their position accordingly.

It’s not quite as straightforward as that – many trend-following managers will employ quite sophisticated “stop-loss” strategies as well, in case the trend they’re backing suddenly goes into reverse – but in essence, systematic trend-following is simply a case of “cutting your losers and letting your winners run”. This might sound easy but, human nature being what it is, cutting your losing positions quickly and letting your winning positions accumulate is actually devilishly difficult to practise successfully.

Most investors, being loss averse, are too eager to take profits on winning positions. By the same token, most investors are too hopeful when it comes to loss-making positions, so they cling on to their losers when the capital tied up in those positions might be more gainfully deployed elsewhere, in a brand new trend.

If this all sounds terrifically risky, it isn’t – at least, not when conducted by a trend-following manager with discipline and experience. Within our own asset management business we do buy trend-following funds as part of our investment process but we don’t invest with new managers – only with managers who’ve been successfully practising trend-following for years, and preferably for decades.

The reason why trend-following is less risky than it sounds is because any decent trend-following manager, all things being equal, is likely to have plenty of “short” positions (selling securities they don’t possess, in the expectation that they can exploit a falling price and cover their short by buying the position back at a cheaper price later) to offset their “long” positions (stuff they actually own in the expectation that its price will continue to rise). And for most of the time, most trend-following funds are actually invested simply in short-term government Treasury bills, because there are insufficient trends in the market to warrant being fully invested. Needless to say, a typical trend-following fund at any given time will also be well diversified by market and by position size and by direction (long versus short).

There are, inevitably, caveats.

Firstly, past performance is no guarantee of future returns. That said, as a signal of a fund’s ability to weather choppy markets, past performance is surely the single most useful attribute that we can go on. Nevertheless, we have to assume that future returns from the sector may not be as impressive as those of the past. We should also bear in mind that trend-following as a strategy doesn’t work year in, year out – and there may be a period of perhaps several years when returns are negative, albeit modestly, compared to equity market ‘corrections’.

Secondly, by dint of being typically structured as hedge funds, it’s not necessarily easy to access systematic trend-followers. Because hedge funds are not regulated, you will struggle to find an investment adviser who can recommend them, and you will struggle to find a fund platform on which you can purchase units in the fund.

If we’ve piqued your interest in systematic trend-following as a form of portfolio insurance, you can always – if you have the risk appetite or the mindset to pursue it – try out trend-following as a trading methodology yourself. If you’d like to learn more about the approach, we highly recommend Michael Covel’s Trend Following, which is a veritable bible on the subject. we also recommend Covel’s excellent web resource, trendfollowing.com.

These are difficult times, and they are likely to get more difficult yet. As part of a diversified and largely defensive portfolio approach, we’re convinced that systematic trend-following funds have an excellent chance of not just surviving the next market shakeout, but actually thriving during the downturn. Aside from the realms of precious metals and real assets, there are no other types of funds that we can say that about with any degree of confidence or conviction.

………….

As you may know, we also manage bespoke investment portfolios for private clients internationally. We would be delighted to help you too. Because of the current heightened market volatility we are offering a completely free financial review, with no strings attached, to see if our value-oriented approach might benefit your portfolio – with no obligation at all:

Get your Free

financial review

…………

Tim Price is co-manager of the VT Price Value Portfolio and author of ‘Investing through the Looking Glass: a rational guide to irrational financial markets’. You can access a full archive of these weekly investment commentaries here. You can listen to our regular ‘State of the Markets’ podcasts, with Paul Rodriguez of ThinkTrading.com, here. Email us: info@pricevaluepartners.com.

Price Value Partners manage investment portfolios for private clients. We also manage the VT Price Value Portfolio, an unconstrained global fund investing in Benjamin Graham-style value stocks and real assets, and also in systematic trend-following funds.

“The game of speculation is the most uniformly fascinating game in the world. But it is not a game for the stupid, the mentally lazy, the man of inferior emotional balance, or for the get-rich-quick adventurer. They will die poor.”

Get your Free

financial review

There is scandal, self-inflicted economic destruction, cultural malaise and political tension aplenty here at home, and no shortage of it abroad.

With a 40-year bull market in interest rates now in the rear-view mirror, and government debt piles now unmanageably vast, we regard the bond markets as essentially uninvestible. Many stock markets are trading at record levels. AI is a bigger bubble than dotcom 1.0. Did someone use the word risky? As Sergeant Esterhaus would routinely say at the beginning of every episode of the TV police drama Hill Street Blues,

“Let’s be careful out there.”

If you were looking for a form of investment that could offer you protection against a multitude of potentially bad outcomes, what would it look like? What attributes would it have? Here are some of the characteristics we would like to see in such an investment:

If such an investment sounds too good to be true, we have news for you.

There is an investment strategy that has been one of the most consistently profitable in the world – for centuries. It is also one of the most secretive. It is mostly used by a small number of traders who happen to know the strategy – but it doesn’t even require huge amounts of capital. And anyone can be taught the basics in minutes.

First, a relevant cultural aside. The movie ‘Trading Places’ was based on a true story.

If you haven’t seen the film yet, you should. It is one of the funniest comedies about Wall Street ever made – not a huge field, admittedly. In it, two unscrupulous commodity brokers wager that they can take a vagrant (Eddie Murphy) off the street and turn him into a successful trader.

The film was a smash hit, symbolic of a more innocent age (specifically 1983) when interference in innocent people’s lives by gambling financiers was the exception rather than the rule.

At precisely the same time, the commodities trader Richard Dennis set out to show that anybody could become a successful trader provided they were simply taught properly.

His partner, Bill Eckhardt, disagreed – and a wager was born.

Dennis placed classified ads in the back of Barron’s magazine. This is what they looked like:

Prior experience was not necessary. But applicants did have to complete a psychological profile. Among the test were some true-false questions, such as:

He ended up with two classes of what he called ‘turtles’, named after a visit to a Singaporean turtle farm. Dennis believed that successful traders could be raised, like baby turtles in a vat of water, simply by being taught the fundamental principles of trading.

And Dennis didn’t rig the experiment. Among those selected for the trial were graduates in piano and music theory, an accountant, a geologist, an unemployed guy, and someone from the United States Air Force Academy. Typical business students they were not.

Long story short, Richard Dennis won his bet.

He hired fewer than two dozen novice traders. Jerry Parker was among them. He is now believed to be worth upwards of $700 million.

$1000 invested with fellow ‘turtle’ Tom Shanks’ Hawksbill Capital in 1988 would now be worth something north of $100,000.

Turtles Paul Rabar, Mike Carr, Howard Seidler and Jim DiMaria all set up fantastically successful trading firms after their experience with Dennis.

So what did Dennis teach them ?

There are only two ways consistently to make money from the financial markets. One of them is value investing. Buying high quality assets for less than they’re fundamentally worth is a credible and immensely successful strategy over the medium term.

The other is what we can call momentum.

Old hands in the City and on Wall Street tend to favour fundamental analysis of the markets. They waste their time discussing and debating the future course of the economy, of interest rates, and inflation. This is all very interesting – perhaps – but fundamentals tell you nothing about how to make money. All of that information is already in the price. And fundamentals are also somewhat subjective – take two economists, ask for their opinion, and you’ll get at least three answers.

Another way to look at financial markets is by using technical analysis. This is not as complicated as it might sound. It simply means looking at the price history of financial assets.

The reality, which is something that Dennis intuitively knew, and that he went on to teach his turtles, is that price is the only metric worth trusting. You can have a view about the future path of interest rates, for example. You may think they’re going lower. But that view might be 100% wrong.

Everything else is subjective.

So this is the system that Dennis taught. It’s a trading strategy that today goes by the title of ‘systematic trend-following’.

‘Systematic’ because there’s a clearly articulated system. This is a rules-based approach to trading. For example, one rule might be:

Another rule might be:

These are clearly simple examples. A decent ‘systematic, trend-following’ system will likely incorporate a wide variety of rules, incorporating guidance on when to get in, when to get out, and how to size positions.

The point being, once you have established that set of rules, you don’t deviate from them. At all. They can clearly be refined, over time. But they should never, under any account, be abandoned.

Unlike many trading approaches, systematic trend-following requires no special understanding of any given market. In fact, we have a friend with a small trend-following fund who assures us that he’s perfectly happy to trade markets ‘blind’ – he doesn’t even need to know exactly what he’s trading, he just needs to see the price history and he can make his trade entry and exit decisions based on that alone.

Trend-followers are not remotely interested in macro-economic analysis. If they use Wall Street research at all, it will be to prop up a wobbly chair leg.

What does interest trend-followers is catching a ride on big market trends. This is the key to the success of trend-following as an investment (more accurately, trading) strategy. Markets have a tendency to make big moves that come as a complete surprise to most investors. But not to trend-followers: big “surprise” moves is precisely what they live for. It’s the source of their outsized profits. Check out, for example, the cocoa price during 2024 for more on this theme.

Today’s trend-followers are following a path laid down by one of the most successful stock traders in history – Jesse Livermore (1877-1940). Livermore’s nicknames included ‘the Boy Plunger’ and ‘the Great Bear of Wall Street’. Livermore managed to make, and then lose, several fortunes. But he was not a creature of some long-lived bull market, like so many of today’s accidentally successful hedge fund managers. After the 1929 Crash, he ended up worth $100 million, when many of his trading rivals lost everything.

Happily for the wannabe trader today, Jesse Livermore’s approach is just as valid as it’s always been. As he said himself,

“There is nothing new in Wall Street. There can’t be, because speculation is as old as the hills. Whatever happens in the stock market today has happened before and will happen again.”

The US firm Research Affiliates published an excellent piece a while ago entitled “How Not to Get Fired with Smart Beta Investing”. You can read it here.

The piece comes to a number of fascinating conclusions about the history of stock market investing over the past 50 years.

For example, it strongly suggests that “quality” and “growth” style investing (essentially, paying up for global mega-brands, for example, or paying over the odds to buy the shares of fast-growing companies) tends to give you worse returns, over time, than simply buying the market.

And it also suggests that there are two strategies that, over time, offer a high likelihood of beating the market. One of them is “value” (which will hardly be news to longstanding readers). The other is “momentum” – which we can define here simply as “buying what’s going up in price – and, for that matter, selling what’s going down”. Clearly they are almost diametrically opposed as philosophies.

“Value” investing is both qualitative and quantitative, and lays great store in patient, defensive, contrarian investing. “Momentum”, on the other hand, is far closer to a shorter term “trading” approach, driven entirely by price; it barely considers the underlying quality of a business at all. Price momentum is really all it’s worried about – what direction the share price is going, and how strong the trend of that share price movement.

So a combination of “value” and “momentum” approaches probably isn’t a bad idea within a balanced portfolio.

How does a systematic trend-following fund actually work? What precisely does it do?

Perhaps 99% of actively managed funds have managers who attempt to predict the future. They try and assess prospects for the wider economy and forecast the direction of interest rates, currencies and inflation (in the hedge fund world this strategy is known as “global macro”). When it comes to the stock market, most fund managers attempt to predict the growth of specific industry sectors or the profits and prospects of individual companies.

Systematic trend-following managers don’t do any of this.

Instead, they simply track the prices of multiple types of assets – interest rates, currencies, stock indices, hard commodities like iron or zinc, soft commodities like corn or soya beans – and when they (or just as likely their computer algorithm) identify a market in something that’s trending strongly (whether up in price or down they don’t really care), they simply initiate a position in that market, and for as long as the trend continues, they will add to their position accordingly.

It’s not quite as straightforward as that – many trend-following managers will employ quite sophisticated “stop-loss” strategies as well, in case the trend they’re backing suddenly goes into reverse – but in essence, systematic trend-following is simply a case of “cutting your losers and letting your winners run”. This might sound easy but, human nature being what it is, cutting your losing positions quickly and letting your winning positions accumulate is actually devilishly difficult to practise successfully.

Most investors, being loss averse, are too eager to take profits on winning positions. By the same token, most investors are too hopeful when it comes to loss-making positions, so they cling on to their losers when the capital tied up in those positions might be more gainfully deployed elsewhere, in a brand new trend.

If this all sounds terrifically risky, it isn’t – at least, not when conducted by a trend-following manager with discipline and experience. Within our own asset management business we do buy trend-following funds as part of our investment process but we don’t invest with new managers – only with managers who’ve been successfully practising trend-following for years, and preferably for decades.

The reason why trend-following is less risky than it sounds is because any decent trend-following manager, all things being equal, is likely to have plenty of “short” positions (selling securities they don’t possess, in the expectation that they can exploit a falling price and cover their short by buying the position back at a cheaper price later) to offset their “long” positions (stuff they actually own in the expectation that its price will continue to rise). And for most of the time, most trend-following funds are actually invested simply in short-term government Treasury bills, because there are insufficient trends in the market to warrant being fully invested. Needless to say, a typical trend-following fund at any given time will also be well diversified by market and by position size and by direction (long versus short).

There are, inevitably, caveats.

Firstly, past performance is no guarantee of future returns. That said, as a signal of a fund’s ability to weather choppy markets, past performance is surely the single most useful attribute that we can go on. Nevertheless, we have to assume that future returns from the sector may not be as impressive as those of the past. We should also bear in mind that trend-following as a strategy doesn’t work year in, year out – and there may be a period of perhaps several years when returns are negative, albeit modestly, compared to equity market ‘corrections’.

Secondly, by dint of being typically structured as hedge funds, it’s not necessarily easy to access systematic trend-followers. Because hedge funds are not regulated, you will struggle to find an investment adviser who can recommend them, and you will struggle to find a fund platform on which you can purchase units in the fund.

If we’ve piqued your interest in systematic trend-following as a form of portfolio insurance, you can always – if you have the risk appetite or the mindset to pursue it – try out trend-following as a trading methodology yourself. If you’d like to learn more about the approach, we highly recommend Michael Covel’s Trend Following, which is a veritable bible on the subject. we also recommend Covel’s excellent web resource, trendfollowing.com.

These are difficult times, and they are likely to get more difficult yet. As part of a diversified and largely defensive portfolio approach, we’re convinced that systematic trend-following funds have an excellent chance of not just surviving the next market shakeout, but actually thriving during the downturn. Aside from the realms of precious metals and real assets, there are no other types of funds that we can say that about with any degree of confidence or conviction.

………….

As you may know, we also manage bespoke investment portfolios for private clients internationally. We would be delighted to help you too. Because of the current heightened market volatility we are offering a completely free financial review, with no strings attached, to see if our value-oriented approach might benefit your portfolio – with no obligation at all:

Get your Free

financial review

…………

Tim Price is co-manager of the VT Price Value Portfolio and author of ‘Investing through the Looking Glass: a rational guide to irrational financial markets’. You can access a full archive of these weekly investment commentaries here. You can listen to our regular ‘State of the Markets’ podcasts, with Paul Rodriguez of ThinkTrading.com, here. Email us: info@pricevaluepartners.com.

Price Value Partners manage investment portfolios for private clients. We also manage the VT Price Value Portfolio, an unconstrained global fund investing in Benjamin Graham-style value stocks and real assets, and also in systematic trend-following funds.

Take a closer look

Take a look at the data of our investments and see what makes us different.

LOOK CLOSERSubscribe

Sign up for the latest news on investments and market insights.

KEEP IN TOUCHContact us

In order to find out more about PVP please get in touch with our team.

CONTACT USTim Price